-

SEBI has mandated that appointment, reappointment and removal of independent directors will have to be done through a special resolution requiring 75 per cent votes as against 50 per cent currently required. There is a dichotomy.

Akil Hirani, managing partner and head of transactions, Majmudar and Partners

Section 100 of the Indian Companies Act, 2013 mandates that a board may within a period of 21 days of the receipt of a requisition notice, received from the shareholders holding at least 1/10 of the paid up shares of the company, carrying voting rights, call a meeting. The EGM is mandated to be held within a period of 45 days since the receipt of the requisition by the board.

On 1 October, the board of ZEE duly met and chose not to hold the EGM citing various grounds including non-compliance under multiple laws, SEBI guidelines, Ministry of Information and Broadcasting, Companies Law and Competition Act. One major issue relates to seeking the prior permission for appointment of directors from the I&B Ministry. Section 25 of the Uplinking and Downloading, Policy Guidelines by Private Satellite TV Channels and Teleports states that no directors can be appointed without the prior approval.

In its communique to the stock exchanges the board mentioned that the decision was made after confirming approval of independent counsels, legal representatives, including senior retired judges of the Supreme Court.

The guidelines also specify that it is obligatory to take prior permission from the Ministry of I&B to effect changes in MD and CEO. SEBI rules also mandate that independent directors requires to be approved by the nomination and remuneration committee and the board. Appointing six independent directors definitely cannot be done without such approval.

Hetal Dalal, president, Indian Institutional Advisory Services (IIAS) a Mumbai-based corporate governance and proxy advisory firm says, “the board, instead of blocking Invesco, will be better placed in engaging with the shareholders having 18 per cent to address their concerns and finding a middle ground, if that is not possible.” To have a meaningful dialogue the board and the other investor need to know what Invesco’s real concerns are.

Darius Pandole, MD and CEO, JM Financial Private Equity says, “Shareholder activism as a concept has primarily been used to protect the interests of minority shareholders, keeping the companies and promoters in check globally. Increasingly, we are witnessing this phenomenon in India as well, as multiple shareholders have started voicing their opinions. Overall this is good for corporate governance in India. However, it is important that this activism should not be misdirected to erode value in the company without adequate justification.” A long drawn battle will erode shareholders value.

There is a dichotomy

The other view is that since Invesco had sought legal remedies, they should approach the board for thrashing out the matter. If there have been serious lapses on the part of the board, the public requires to be told about it. They have made their point and two directors have already resigned prior to the AGM. Pursuing a legal battle for the removal of MD and CEO, who was duly appointed by the shareholders in 2020, will only be time-consuming. “NCLT’s order is also subject to further appeal.” says Akil Hirani, managing partner and head of transactions, Majmudar and Partners, a full service legal firm. “Calling of list of all shareholders and subsequently calling an EGM will lead to further protraction.”

SEBI had in March, earlier this year mandated that appointment, reappointment and removal of independent directors will have to be done through a special resolution requiring 75 per cent votes as against 50 per cent currently required. The Companies Act 2013 which deals with the appointment and removal of directors has not been amended as yet. “There is a dichotomy,” says Hirani adding that “the Ministry of Corporate Affairs requires to resolve it.”

While there are several such legal and technical issues which may nullify the requisition one will have to wait for the order of the NCLT on 4 October to see what further directions are given. The declaration sought in the civil suit in Bombay High Court is an independent proceeding and is unlikely to be decided in a rush. The High Court also has supervisory jurisdiction over NCLT.

-

While the grounds for Invesco’s aggressive initiative is not clear, speculations abounds as to why Invesco is doing what it is doing. (See box: What has peeved Invesco?) Any rational investors would, short of jumping with joy, be at least pleased at the development hoping the merger with Sony would spell good news for everyone. A non-binding term-sheet with Sony Pictures Networks India (Sony) was approved by the board. The broad contours in the term-sheet envisaged Sony bringing in capital to the tune of $1.58 billion (Rs11,700 crore). The funds would be utilised for bidding for IPL rights (currently with Star), creation of content and improve digital platforms of Zee5 and SonyLIV.

Currently both these platforms are trailing. Sony would be the major partner having 53 per cent in the merged entity while Zee would hold 47 per cent. Goenka would continue as the MD and CEO for a period of 5 years but Sony will have the right to appoint members on the board of the merged entity. While it is not clear what role N.P. Singh, the current CEO of Sony will play, there is a good chance that he may be on the board of the merged entity.

Business India had spoken to a number of persons soon after the announcement of the proposed merger. The mood was jubilant. “It is a fantastic deal,” exclaimed Ajay Garg, Investment banker with 22 years of experience, currently the MD, Equirus Capital Pvt Ltd, a full-fledged financial service company. “The merger is the best thing for Zee and I do not foresee the majority of rational shareholders opposing it.”

Garg explains that for the Zee group which was defocussed due to other problems in the group, this deal will again ensure focus on growth in its areas of strength viz producing and distribution of content for TV through its channels across 175 countries. Sony will also bring to the table its international expertise in production of movies, sitcoms and live content to the table. He adds, “The money that it gets in the company can be used to build OTT platforms and create more content besides strengthening its leadership across segments in the Media and Entertainment stage.”

Wide reach

Zee, which is totally focussed on entertainment since 2016, has probably the widest reach in India with a good penetration in smaller cities and towns. It also has a good library of movies. Sony on the other hand is more focussed on urban viewers. It has also got a good bouquet of sports channels. Ten Sports was incidentally taken from Zee in 2016 in an all cash deal for Rs2,600 crore valuing the sports business at 4x its revenues of Rs630 crore. Zee Entertainment then had a market cap of Rs54,000 crore (Business India, cover feature on Sony, January 30-February 12, 2017). It has good sitcoms and family serials shown on Sony SAB. The merged entity would have nearly 75 channels, 2 video streaming platforms, 2 production studios, 1 video offering diverse content in sports, entertainment across various languages in 175 countries.

-

Had Sony not adopted an aggressive approach in bidding for Zee now, they ran a threat of losing market share and dropping to no. 4 position in case Network18 acquired Zee

Deven R Choksey MD, KR Choksey Investment Managers

With changing trends with a discernible shift to digital and consumers increasingly seeing live programmes on their mobile, there has been a shift in which consumers are viewing the content. While both ZEE and Sony have their video streaming platforms, Zee5 and SonyLIV, the two are trailing far behind Star Sports in term of subscribers. Star has an estimated subscriber base of 39 million. This is nearly 3x the combined subscriber base of Zee5 and SonyLIV.

The money which Sony brings in the merged entity would help them to bid aggressively for getting the IPL rights, one major draw for cricket buffs, many of whom subscribe to Hotstar solely to watch IPL matches in peace either in the homes or travelling. Undoubtedly the merger of an international company with an Indian giant works well for both as and when it happens says, H.V. Harish, managing partner, ECube Investment Advisors. Both have their strengths and Sony is bringing in capital which should be beneficial to the combined entity.

“However as of now it is a tricky situation. If Invesco succeeds in calling an EGM to oust Punit Goenka, it has to muster support from other shareholders. In order to succeed, Invesco needs to put an alternate plan of action for Zee so that shareholders can compare it with the one proposed by the current management with Sony. That would give shareholders a clear choice to make.” Pointing out that while this is good from a corporate democracy and governance perspective for the country that boards are challenged and alternate proposals given.

One does not know for sure if Invesco is in favour of the deal or against it. If they have an alternate proposal they are keeping it closely guarded to themselves. One grouse they have is that Sony has asked Goenka to helm the merger and remain as MD and CEO for next 5 years. The other could be that their shares would be diluted and become less than half in the merged entity. Sony has also offered to give 2 per cent shares to Goenka in lieu of signing a non-compete agreement which would allow it to retain 4 per cent in the merged company. By way of a sweetener Sony has given an option to promoters to raise their stake in the merged entity to 20 per cent.

More suitors waiting

Invesco could only have been consulted after the public announcement. The timing of the announcement has also raised eyebrows. While the negotiations must have been done over a long period of 6-7 months the announcement was made within days of receiving the notice to remove the directors including MD and CEO.

Deven R Choksey, MD, KR Choksey Investment Managers, points out that “Star is the undisputed leader currently in GEC and news channels. Viacom 18 which is a part of Network18 of Reliance group, has a strong bouquet of channels. Had Reliance made an offer to acquire ZEE now, which it reportedly did a couple of years back, Sony could have been marginalised.” Had Sony not adopted an aggressive approach in bidding for Zee now, they ran a threat of losing market share and dropping to no. 4 position in case Network18 acquired Zee. Zee has the best penetration in the country as also with the Indian diaspora in 175 countries. It has also made deep inroads in regional languages. For RIL strengthening media presence under broadcasting and internet segments is key to gaining market share.”

While there have been talks that other financially strong companies including RIL or Adani as possible suitors for Zee. Choksey emphatically states “RIL will not settle for other than majority stake in Zee. In case the said merger doesn’t go through for any reason, I do not rule out RIL getting into the game.”

-

The key task for the board currently is to negotiate with Sony and if possible get better terms for all its shareholders. After all, the merger will also provide Sony a ready avenue to merge in a listed company. Even as the battle lines are drawn there is nothing to stop the two warring parties from holding without prejudice meetings to arrive at an amiable settlement. Shailesh Haribhakti, a strong votary of corporate governance and chairman of Shailesh Haribhakti and Associates, says, “A well constituted board will safeguard the interest of all stakeholders.” Haribhakti is also appreciative of the Zee-Sony merger.

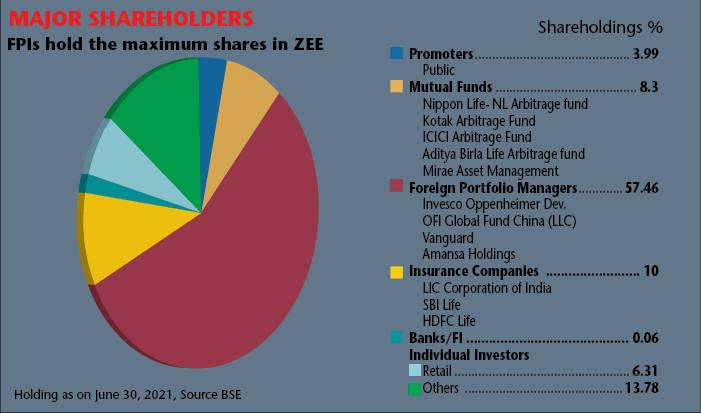

As of now the merger issue has been put on the backburner. The total focus is diverted from the growth of the company to the fight between Invesco, the largest shareholder and Punit Goenka – its MD and CEO who had brought the company to its present stage. The other shareholders besides the 22 per cent held between Goenka and Invesco, do not seem to have too much of a clue about what the fight is all about.

While investors have rights to raise issues in the company, the fact remains that the promoters are the ones who have an equity of their own as long as there is no mismanagement or impropriety. If the contentious issues are not resolved amicably, there is every likelihood of the merger being derailed. The next few weeks could probably throw more light.

-

The merger is the best thing for Zee and I do not foresee the majority of rational shareholders opposing it.

Ajay Garg MD, Equirus Capital Pvt Ltd

Why is Invesco peeved?

Invesco’s relationship with ZEE goes back to at least two decades. Even in September 2007, Oppenheimer Funds A/c Oppenheimer Global Funds held 3.82 per cent stake in Zee. They have been gradually increasing their stake. In September 2008 Oppenheimer Developing Markets Fund and Oppenheimer Global Fund held 5.52 per cent stake in the company. In 2019, Zee was facing a problem due to a pile up of debt at the group level. On 25 January 2019, when the group defaulted, Subash Chandra in an open letter apologised for the non-payment and stated that all his group companies are doing well and the debt burden is purely at the promoters’ group level for the infrastructure business (housed in Essel Infrastructure).

Chandra in his letter stated, “For the first time in my career of 52 years, I am compelled to apologise to our bankers, NBFCs & Mutual Funds, since I believe that I have not lived up to their expectations, despite the best of my intentions. I am extremely certain that there is no promoter in India Inc., who has dared to sell the jewel of his crown, to pay off the liabilities.”

Zee share prices which were under pressure tanked by nearly 33 per cent from the closing of Rs434 on 24 January to a mid-session low of Rs289. Chandra’s assurance apparently stemmed further downslide as several mutual funds withheld their sales. Only one mutual fund had sold its stake to recover its dues prior to 25 January. The volumes traded on BSE were also high in the week. The volumes on 25 was Rs200 crore which doubled on 28 January. Delivery ratio to volumes was also very high during the week with the highest being at 72 per cent on 23 January, probably the day one mutual fund offloaded the value. Chandra has asked time till 30 September to pay off all dues. This stemmed further sales from mutual funds.

Prior to this date in the period from 20 September 2019 to 26 September a similar trend was noticed in the markets with heightened volumes and high delivery to volumes traded were witnessed.

This was the time when Disney formally took over Star India and its associate companies including Hotstar. At a time when Chandra and his team were desperately seeking to offload their shares and Comcast was also willing to come in with riders, of course, Invesco sought to further increase their stake by buying another 11 per cent for Rs4,224 crore from the promoters in July. Strangely the shareholding of Invesco Developing Market Fund and OFI Global China Fund have remained virtually constant, at 7.74 and 10.14 per cent save for a small dip reported in OFI Global China Fund which at the end of September was 8.70 per cent. There is no publicly available information about any promises if any made to Invesco at the time of purchase about reducing guarantees or related parties deal.

It is still not clear what has miffed Invesco at this stage.

While Invesco has not openly rejected the Sony deal it apparently wants an independent board to evaluate the deal. However, one can question whether the 6 proposed nominees are the best people to judge. Some analysts also feel an independent board could also invite bids from other strategic investors.

Mukesh Ambani is not known to overpay for assets and being in the business of broadcasting may not want to get into an open bidding warfare game. Unless Invesco gives another option, there is a good chance that Zee will be able to muster majority votes. One view is that Zee can even opt to have a combined resolutions put at the EGM, the first part to support the merger and second one to reiterate the confidence in Goenka.