-

India will produce an estimated 27 million tonnes of sugar. This is lower than the 33.1 mt produced the previous year

This level of sugarcane is more than enough to meet the yearly domestic consumption of 25 mt. For 2019-20, Covid-19 is expected to reduce consumption to between 0.5 mt and 1 mt. By and large consumption has remained unchanged for the past many years due to the changing dietary habits in tune with global trends.

Besides consumers, institutional sales, which constitute around 60 per cent, include sales to confectionaries, pharma companies, chocolate manufacturers and distilleries. Along with this year’s surplus, the 14.5 mt carried forward stock from last season would have seen the industry reeling under this burden.

However, the government has taken various steps to ensure stability in prices. It took a decision to keep a buffer stock of four million tonnes (mt), for the year ending 31 July 2020 for which it would reimburse the cost for storing the inventory. It also came out with a policy (Maximum Admissible Export Quantity) to allow eligible mills to export a total of six mt during the sugar season. A monthly release mechanism has also been put in place to ensure that too much supply would dampen prices unnecessarily.

It has also incentivised mills to produce ethanol from the pulp of various varieties (B+ which has a higher sugar residue, C+ and even directly from the juice). The prices are remunerative and vary from Rs59 to Rs43.75 per litre. In a bid to facilitate exports, the government will spend nearly Rs10,500 crore of which the Central government’s share will be Rs6,268 crore. Storing 4 mt would set it back by another Rs1,600 crore or so.

While the measures are good and will help sugar companies deal with excess inventory, the fact remains that but for the government’s intervention the industry would not have been able to export sugar. In the global markets, raw sugar is currently priced at 11.7 cents to a pound which is roughly Rs20 per kg. Sugar with ICMUSA (an international unit for measuring the purity of sugar in solution and is linked to the whiteness of the material) of 45-50 would fetch a few cents more. In India most of the sugar is termed between 100-150 IC.

-

Tarun Sawhney: ethanol cannot solely be the long-term panacea

Government intervention

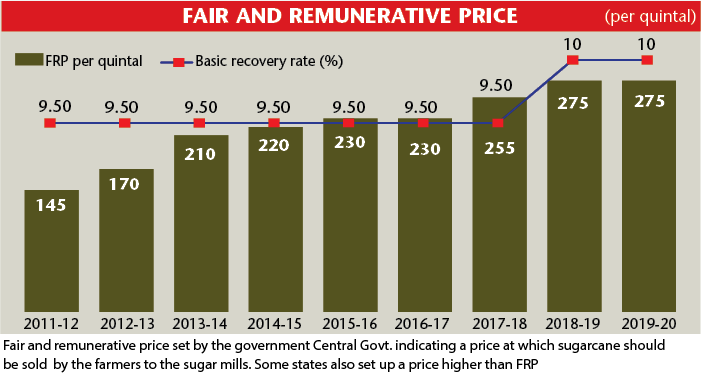

The reason for Indian sugar being non-competitive in global markets is the total intervention of the government – right from the procurement of cane to fixing the prices. In a bid to ensure that farmers get a reasonable price based on the risks they take, the government announced a Fair Remunerative Price (FRP) as it is called. This is based on the Recommendations of the Commission for Agricultural Costs and Prices, in consultation with the state government and industry body, ISMA.

Over the past 10 years, the FRP has gone up from Rs145 per quintal of cane in 2011-12 to Rs275 per quintal in 2018-19 and 2019-20. The price is linked to the recovery of sugar from the cane. The benchmark for the current season has been fixed at 10 per cent. In case of a higher recovery, the prices go up by Rs2.75 per quintal for every 0.01 per cent addition over 10 per cent. In case of recovery of less than 10 per cent a similar deduction is allowed subject to a minimum price of Rs261.25 per quintal being payable even if recovery is less than 9.25 per cent.

Besides the FRP fixed by the Central government, in some states, a State Advisory Price (SAP) is also given. This is invariably higher than the FRP price. In Uttar Pradesh it ranges between Rs310-325 per quintal. The higher price is applicable for the fast-growing crop variety.

To balance the higher price, the government also fixes a higher price for selling sugar. The maximum selling price is currently at Rs31 per kg. Other varieties of sugar like sulphurless sugar, is priced a little higher. As of now only a few companies like Shree Renuka Sugars and Mawana Sugars are making this variety.

-

Another criticism is that India is not a regular exporter. It chooses to export only when there is a surplus

The fact that the industry is high-cost is known to the government, which over the past few years has been seized of the problems and is also supportive of the industry. However, in a bid to appease farmers, the government has no option but to keep increasing prices. No government, after all, would like to incur the wrath of 50 million farmers.

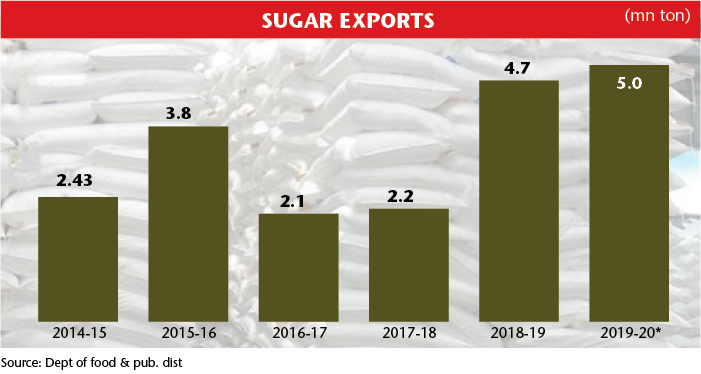

Another criticism is that India is not a regular exporter. It chooses to export only when there is a surplus. This ad-hocism in exports goes against the country. “There is a need to have a consistent export policy. This will help exporters ink long-term annual contracts. India also needs to tap new geographies,” says Anuj Sethi, senior director, Crisil Ratings.

Given the current surplus scenario, which is likely to continue over the next few years, this may well be an ideal year for the government to frame a new export policy. By announcing it before the beginning of the sugar season, it would allow companies to better manage their inventories and liquidate stocks. Major countries importing sugar include the US, China, Italy, Spain, Sudan, Iran, Bangladesh and Algeria.

Announcing an FRP in advance, however, allows liquidation of cane arrears as government support is invariably given directly to farmers to cut their dues. In sugar season 2018-19 almost 95 per cent of the sugarcane farmers’ arrears of Rs86,673 crore has been paid off. This too on SAPs. “Structural changes are required to be ushered in the sugar industry,” points out a senior executive of a large company. He suggests that there should be only one price for cane fixed by the Centre. SAPs should be done away with.

-

State governments are buying sugar through open market purchases. Photo credit: Sanjay Borade

Rangarajan Committee Report

The Economic Advisory Council headed by C. Rangarajan, former RBI governor, in its report on the Regulation of the sugar industry – The Way Forward, suggested ways and means to improve efficiency and promote investments in the sector. Submitted in October 2012, the committee recommended the deregulation of the industry. It pointed out that even though India produced 17 per cent of the global output, its exports amounted to less than 4 per cent of the global share. It recommended doing away with quantitative restrictions and instead the usage of tariffs to balance demand during shortages.

It further suggested that over a period of time states should encourage market-based long-term contractual arrangements between farmers and mill owners and phase out cane reservation area and bonding. As per the arrangement, persisting even today, farmers within a 15 km area have to sell their output to the specified mill within the area at a price specified by the government.

The farmer is forced to do that even if the mills do not make timely payments and it also curbs the mills’ flexibility of buying from areas it chooses. It also mooted doing away with restrictions placed on the mills for the sale of its molasses and bagasse. Currently, in UP, for instance, the state reserves the purchase of 18 per cent of molasses at a fraction of the market rate for distilleries to make potable alcohol. Liquor is a good revenue generator, allowing distilleries to get molasses at a lower rate helps the state’s exchequer. It recommended no restrictions on byproducts.

The only major recommendation followed by the government was abolishing of the dual control of levy pricing and open sales. Doing away with levy prices, state governments are currently buying sugar through open market purchases for onward distribution to the weaker sector at a concessional rate. The government bears the differential loss.

-

Ethanol

Currently, the government has incentivised sugar companies to set up distilleries to produce ethanol as a by-product from the molasses left after squeezing juice from the cane. It has mandated that government oil marketing companies (OMCs) should use up to 10 per cent ethanol as an additive to the petrol marketed by the OMCs. It plans to gradually increase it to 30 per cent by 2030. A subvention scheme for allowing companies to take loans for setting up refineries has also been put in place. The pricing of ethanol is not made public but periodic tenders for ethanol are floated at a varying rate.

Brazil, which like India was once dependent on oil imports, had nearly 20 years ago allowed sugar companies to produce ethanol to lower inventories and also use it as an additive or use it as a 100 per cent substitute to petrol. The prices of both ethanol and petrol were subject to market forces and varied from day to day, giving consumers the option to switch to the fuel of their choice. The country, which at that time did not make any automobiles, persuaded auto companies to make flex cars allowing flexibility to use either fuel of choice.

In India, though the government has allowed companies to set up refineries, very few sugar companies have good balance sheets to offer a bankable project. Out of an estimated 363 companies which had shown interest, only 53 projects got approval and only 35 got disbursement to set up ethanol refineries. The average pay-back period for an ethanol refinery is six years, which is too much, given the cyclicity of the industry, confides one top industrialist. Getting 10 per cent of the industry is also a problem.

“Ethanol cannot solely be long-term panacea. The linkages between sugarcane price and sugar price are the heart of the solution,” says Tarun Sawhney, vice-chairman, and MD, Triveni Engineering Industries, one of the largest integrated sugar mills which produced a record 1 mt of sugar in FY20.

Sawhney, who is also the chair of the CII National Task Force for sugar, ethanol and also biogas, says that a higher pricing of ethanol and free movement of ethanol and molasses even within the state could spur investments in ethanol, even from non-sugar companies. The company, during the Covid-19 period started manufacturing sanitisers.

-

Vijay Banka: we need an ambitious plan

“We need an ambitious plan for manufacture and use of ethanol,” says Vijay Banka, MD, Dwarikesh Sugar Industries. Banka points out that in “Brazil in the last crushing season, 65 per cent was used for the manufacture of ethanol and only 35 per cent was used for the manufacture of sugar.” Banka feels that a concerted move to permit higher manufacture of ethanol will allow for the liquidation of the pile-up of stocks in the industry.

“It is desirable to support integration and allow sugar companies to build economies of scale,” says Roshanlal Tamak, executive director and CEO, sugar division, DCM Shriram, a diversified company with exposure to sugar. DCM Shriram, which has two distilleries, has gone in for forward integration and set up an 11,000-case country liquor bottling plant to allow the company to swing capacities between ethanol and liquor. Tamak feels that a “long-term policy in pricing of ethanol will help the industry in setting up more capacities.” Dhampur Sugar, another integrated sugar company having amongst the largest distilleries (400,000 litres per day) has also gone in for manufacturing country liquor and sanitisers.

Besides ethanol, companies are also allowed to generate power from bagasse, another by-product. Most leading companies have invested in setting up power plants. Dhampur has a 220 megawatt (MW) power plant. Power tariffs are fixed on a five-year basis. However, in UP due to lower demand for power, the distribution company took the unilateral decision to reduce the price paid to sugar mills as much as 40 per cent per unit.

The sudden change has caught the industry unaware, with many companies seeking legal redress. From a rate of Rs5 per unit the prices have been slashed to Rs2.95-3 per unit resulting in a near 40 per cent decline in the income of the sugar industry from power. Power from ethanol accounts for around 10 per cent of the total income. A majority of the income comes from the sale of sugar. Some companies have started selling branded sugar in packets which have resulted in somewhat higher margins. However, the bulk of sugar is sold loose.

-

Some companies have started selling branded sugar in packets but the bulk of sugar is sold loose

Consolidation

Given the prevailing situation in the industry, there are several companies operating single refineries making losses and unable to even service debt. Most sugar companies have taken debt both for meeting working capital and capital expenditure. However, the weak ones are unable to even meet payments to farmers.

Given the structure, farmers are forced to sell to the designated mills even if there are arrears and mills use the credit as working capital. While consolidation within the industry is an ideal situation, it is not happening, certainly not of late. Cane prices are lucrative and guarantee that farmers look at sugarcane as a crop of choice.

Some companies, on the other hand, are extremely efficient and paying shareholders through regular dividends and buy-backs. “We have kept debt under control and managed to retain our focus on growth,” says Pramod Patwari, CFO, Balrampur Chini. Patwari is appreciative of the government’s ethanol policy of allowing ethanol to be produced from molasses, B+.

Some units in the South are closing down due to the paucity of supplies of cane sugar due to successive crop failures. This is more out of compulsion and is seen in those companies having mills at multiple locations across various states. However, many weaker players with poor balance sheets are still surviving.

-

The future

The government is all set to announce new prices both for cane and sugar for the coming year which will start in September. There have been various media reports speculating over a possible increase in the price of sugar by at least Rs2 per kg. This is also a demand made by various industry bodies across states. Abinash Varma, director-general, Indian Sugar Mills Association (ISMA), points out that the last price was fixed in January 2019. “The price fixed by the government did not take into account the interest cost which sugar mills have to pay for servicing their working capital and term loans. It ignores depreciation.

Besides, the processing and conversion cost is based on the most efficient company’s data which should be based on the average conversion cost of the industry,” he says. Some experts also fear that the government may also increase the FRP for farmers to Rs285 per tonne.

In most cases, cane forms nearly 80 per cent of the cost. In the bad years it goes as high as 90 or sometimes over 100 per cent, says another industry person. However, it will be a while before cane-linked sugar prices – subject to the satisfaction of both farmers and industry – are arrived at. The solution lies in decontrol across the value chain, as recommended by the Rangarajan Committee. There have been suggestions by several companies for creating a price-stabilisation fund which could be funded by levying a small tax on the end product of sugar.

This could be used to balance price fluctuations during good and bad times. A similar fund could also be created to help farmers during bad times. However, no state as of now seems to be inclined to move in that direction, and dichotomy of prices for cane by the Centre and states still remains. The solution lies in laying out a road map to move in that direction if not now, at least over the next five to 10 years period. Till such time, sugar will continue to remain a volume play.