-

Gold era

Fedfina has made its mark in the gold loan segment. Gold loans have been gaining popularity since 2008, and account for 11 per cent of overall retail loans in Fiscal 2021. In fact, as can be seen from the growth rates of several NBFC peers, the industry has grown consistently over the last decade, even as gold prices have fluctuated periodically. CRISIL Research estimates the outstanding value of loans given out by financiers, that is, banks and NBFCs, to be Rs4.7 lakh crore, with NBFCs accounting for one-quarter of the market.

A sizeable portion of Indian households’ physical assets is gold, which continues to grow. In fact, the gold of Indian households has increased from about 20,000 tonnes in FY11 to about 27,000 tonnes as of FY21, higher than China and US official gold reserves. However, only about 7 per cent of this gold is pledged with financiers, according to CRISIL Research. With more households and small entrepreneurs monetising gold, the high private gold holdings means that the addressable market is huge.

Fedfina is customising solutions for gold loan customers. Umesh Vithal Thakkar, a government contractor providing manpower for road laying and pedestrian pathways for the local government of PMC and PCMC in Pune, needed a loan to expand his manpower requirements. Thakkar was unable to secure funding from mainstream and larger financiers due to the sporadic cash-flow inherent in his line of business. Fedfina understood his requirements and, after due diligence, provided him a gold loan with which he could expand his business.

Besides, with the average price of Rs46,579 per 10 grams of gold in September 2021, monetising even 20 per cent of the gold stock in the form of loans at a 70 per cent loan-to-value ratio leads to a Rs17.6 trillion market opportunity for financiers, notes CRISIL Research, which expects AUM to grow at 13 per cent CAGR between FY21 and FY25.

Of the gold-loan NBFCs, those like Muthoot Finance and Manappuram Finance target customers at the lower end of the economic strata with an average ticket size of approximately R44,500 and yield of 22-25 per cent. On the other hand, Fedfina caters to lower middle-class and middle-class customers with an average ticket size of R1,00,000 and an interest rate of about 18-20 per cent.

Underserved segment

Another area where Fedfina has a strong presence is the MSME loans segment. With a visible demand-supply gap, especially in the lower ticket size, MSME lenders are focussing on the underserved segment, translating to growth opportunities for financiers such as Fedfina.

Less than 15 per cent of approximately 70 million MSMEs have access to formal credit of any sort. The perception of higher risk and high cost of delivering services have seen traditional financiers going slow in providing credit to under-served or unserved MSMEs and self-employed individuals. This segment usually resorts to credit from informal sources. Hence, this segment is an untapped market which offers NBFCs good growth potential too.

Fedfina has been serving people like Bharat Yadav. The tea stall, snacks and pan parlour vendor has been operating at a prime location in Waghawadi Road, Bhavnagar, for 20 years. Yadav required funds to expand his product offerings and renovate the store. Bharat had a self-occupied residential property at a prime location in Bhavnagar, valued at Rs29 lakh.

Fedfina’s sales and credit team spent time with Yadav and assessed his business and daily turnover, simultaneously checking with major wholesale suppliers to arrive at his monthly income. Yadav had also serviced a prior loan well, and Fedfina sanctioned a small ticket LAP of Rs16 lakh with a loan-to-value of 55.17 per cent and an EMI of Rs33,812 a month.

-

Ganesh: better risk profile; Photo: Sanjay Borade

CRISIL Research points out that MSME loans with ticket sizes of between Rs10 lakhs and Rs1 crore are expected to clock a 15 per cent CAGR over Fiscals 2021 and 2025, aided by increasing lender focus and penetration of such loans, enhanced availability of data increasing lender comfort while underwriting such loans, enhanced use of technology, newer players entering the segment, and continued government support. “We have a vast product suite that provides us with the platform to gain from this expected growth,” says Kothuri.

Fedfina has, in fact, built a large presence across India, which should stand it in good stead in tapping under-penetrated markets. It has operations in 15 states and Union Territories, and is strong in southern and western India, which covers more than 75 per cent of India’s GDP. Its 463 branches are located in strong markets, which tend to have better asset quality than other states, notes CRISIL.

The firm has also been harnessing technology to bring about efficiency in targeting the right segments and improving lending practices. Fedfina introduced a ‘Phygital’ doorstep model, which is a combination of digital and physical initiatives. Fedfina employees carry out appraisals and instant disbursals at customers’ premises, before transferring the pledged gold to a nearby branch with in-transit security, which includes an electronic safe with GPS for tracking. The company further utilises multi-tier authentication, as well as online portal and mobile applications for real-time tracking and 24/7 customer service.

Technology investments also aid in managing scale and size. The firm’s technology stack has customised tools and applications that enhance operational efficiency, automation and customer convenience. In the half-year FY22, the firm invested over Rs8.7 crore in technological investments, which is more than twice the investments made in FY21 of Rs4 crore.

Low delinquencies

Fedfina has a stringent underwriting process which combs through the vast data customers generate using digital platforms. The firm rigorously validates the data to assess the customer’s creditworthiness. So even while the firm focuses on the underserved category of the Indian loan market, Fedfina follows prudent customer selection policies with more than 78 per cent of its borrowers having a high CIBIL score.

Needless to say, over the years, the firm has maintained a good handle on non-performing loans. “We believe that our risk-management policies have resulted in our healthy asset quality and low credit costs. Our underwriting process has allowed us to manage and reduce defaults and NPAs across all our products in FY12, FY20 and FY21. Our gross NPA was 2.22 per cent and 1.01 per cent for the six months ended 30 September, 2021, and FY21, respectively while net NPA was 1.60 per cent and 0.71 per cent for the six months ended 30 September, 2021, and FY21,” says Kothuri.

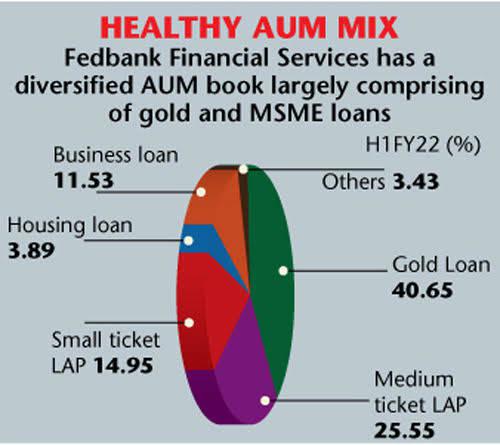

Besides, the AUM mix is well-diversified against gold, and loans against property (LAP). Fedfina’s gold loan AUM as on 30 September, 2021was 40.65 per cent, 25.55 per cent for medium-ticket LAP, 18.84 per cent for small-ticket LAP and housing loans, and about 11.53 per cent for unsecured business loans. One of the good things is that the retail nature of its business cuts the industry concentration risk in its business.

-

One of the keys to a successful lending business is the low cost of borrowing. On that count, Fedfina is doing quite well. Its ability to access diversified sources of funding has been a key contributor to its growth. Its strong parent in Federal Bank means the firm has access to a good source of capital. Besides, it has secured financing from lenders such as banks, financial institutions, mutual funds and sources such as term loans.

Its high credit score and diversified borrowing program have led to its average cost of borrowing of about 7.75 per cent as of 30 September, 2021. This ranks as one of the lowest costs of borrowing among MSMEs and gold-loan peer-sets, notes CRISIL. Fedfina is rated AA- for its NCDS and long-term bank facilities. “Our ability to borrow at a comparatively lower cost of funds than peers permits us to chase a better risk profile of borrowers among MSMEs with more competitive rates. This in turn has resulted in comparatively lower NPAs in the retail book even during the Covid years,” says C.V. Ganesh, CFO at Fedfina.

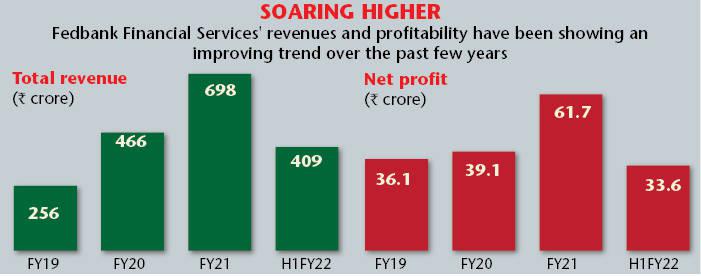

All these investments have resulted in a significant expansion in its business operations. Fedfina’s revenues grew from Rs255.5 crore in FY19 to Rs697.5 crore in FY21. On the other hand, profit after tax expanded from Rs36.1 crore in FY19 to over Rs61.6 crore in FY21, more than doubling. Overall assets under management have also raked in strong growth, rising from Rs2,019.2 crore in FY19 to Rs4,862.4 crore in FY21, which is commendable. For the half-year September FY22, AUMs jumped to Rs5,246.7 crore. Further, Fedfina has expanded its net interest margin by more than 200 bps to 8.69 per cent for the six months ended 30 September, 2021, over 6.58 per cent for Fiscal 2019.

While growth has been good, Fedfina is eyeing a bigger share of the growth pie. As a part of its capital augmenting strategy, it is proposing to issue equity shares to augment its Tier 1 capital to meet future capital requirements arising out of the growth of its business and assets. Its Tier 1 capital adequacy was 25.63 per cent as of 30 September, 2021, and will be significantly augmented, post-issue.

With retail loans, particularly gold and small and medium business loans showing huge promise, the additional capital will not only strengthen the balance sheet but also provide capital for growth. “We have delivered consistently and have industry-leading performance across various benchmarks, such as AUM growth, NNPA and GNPA levels and cost of funds”, says Kothuri aspiring to continue to deliver consistently on leading return matrices.