Golden era

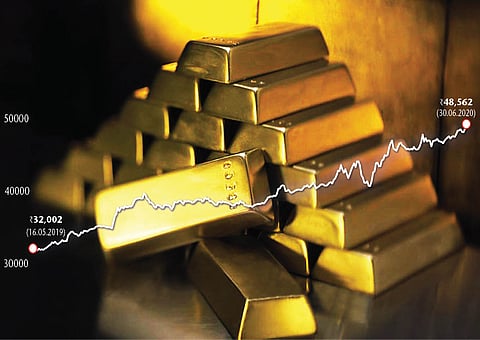

Yes, the yellow metal is on a roll. On 5 July 2020, spot gold rose 17 per cent, closing out the second quarter of the year, with the largest rally in more than four years. The latest Goldman Sachs analysis raised its 12-month forecast on gold to $2,000 an ounce, from $1,800. It also lifted its three-month view to $1,800 from $1,600 and its six-month forecast to $1,900 from $1,650. The question is: will it get there?

If one recalls, in September 2008, in the US, after the collapse of Lehman Brothers which led to a worldwide economic crisis, gold jumped from around $700 an ounce to peak at around $1,900 an ounce in September 2011. In the next four years, it declined to nearly $1,000 an ounce. Between 2015 and 2019, gold remained in the range of $1,000 and $1,350 an ounce, after which it has started a steady run.

“The price of gold has been on an upswing since August 2019, as a result of several factors. A 180-degree shift in US interest rates, unprecedented levels of sovereign debt in the negative yield territory signalling concerns on global economic growth, trade wars and several pockets with geopolitical tensions,” says Somasundaram P.R., MD (India), the World Gold Council.

“In uncertain times, gold becomes the most attractive investment. Also with the dollar being weaker, the inverse relation with gold holds. With a global recession being forecast this year, financial instruments become less reliable for investors while gold becomes attractive. Further, as a long-term investment, this is the right time for people to buy gold and this is why demand has gone up since the beginning of the year even before Covid-19 which has only accelerated today,” says Madan Sabnavis, chief economist, CARE Ratings.

“In the past 20 years, gold has given a return of almost 15 per cent. It’s an easy commodity and can be encashed anytime, anywhere and any place. The gold prices have become more transparent, so there is no question of cheating in price. We can see that every year there is an appreciation in gold price and in last year it was almost 30-35 per cent,” says Prithviraj Kothari, national president, India Bullion and Jewellers Association Ltd (IBJA).

He feels that gold prices rise due to the increase in international prices and also because of the instability in rupee vis-a-vis dollar. In India, the biggest focus is towards the demand and not the price. If the market is high then the demand is more towards buying. We were under the impression that due to Covid-19 outbreak; one will come to the jeweller to sell gold and take profits.

However, it has been observed that people have started buying gold and jewellery in spite of gold price being at an all time high. “From my personal 35-40 years of experience, I can say that when gold prices are high, demand rises and when price falls, demand falls because people are under the impression that the price will reduce more and they wait for the right price,” adds Kothari.

“The rise of gold prices in dollar terms is the main reason for the rise in prices in India. Basically, the lowering of interest rates on dollar deposits makes it less attractive vis-a-vis gold where the expectations of returns are higher due to global uncertainty. Pandemic and revision of growth forecasts are the main reasons of high uncertainty worldwide,” adds Ketan Kothari, director, Augmont, an integrated precious metals management company.

The prices of this metal are affected considerably by the international markets. “Uncertainty is the perfect recipe for higher gold prices. The current narrative backdrop fits the bill for bullish gold prices, characterised by Covid-induced deceleration in growth,” says Hitesh Jain, lead analyst (institutional equities) at Yes Securities. He sees the world GDP contracting by 3 per cent this year, “such contraction was not seen since decades. Moreover, expansionary monetary and fiscal policies are also supportive for the yellow metal. On the monetary aspect, central banks have done nothing short of throwing the kitchen sink,” adds Jain.

During the subprime crisis, the Fed balance sheet took six years to double from $2 trillion to $4.5 trillion. Now, Fed takes six months to expand its balance sheet from $4 trillion to 7 trillion to counter the economic consequences of Covid. The combined value of the Fed, BOJ and ECB balance sheet is at $19.5 trillion from $14.7 trillion during the beginning of the year. On interest rates, Fed has proclaimed to keep interest rates static, close to zero till 2021 end. Although Fed has ruled out negative interest rates, real interest rates have turned negative. On the fiscal side, global stimulus is widening budgetary shortfall to an unprecedented level. The US fiscal deficit widened to $1.88 trillion for the first eight months of this fiscal year – at an all-time high.

The US fiscal deficit has widened to 10 per cent of the GDP from 4.7 per cent at the end of 2019. “It’s clearly a hand-in-glove relationship between governments and central banks: Central banks will print money to finance the federal deficit. Monetary debasement of fiat currencies increases the safe haven appetite for alternate currencies like gold. Faltering world trade, de-globalisation, rise of nationalist political parties across the globe are also supportive for gold.

Japanification of the world: Real interest rates turn negative in Europe and US. Non-yielding gold is now a better instrument than negative-yielding bonds. In a $36 trillion global government bond market, market value of sub-zero yielding bonds is at $13.5 trillion,” observes Jain.

India is one of the largest consumers of gold and as such any kind of movement in its prices internationally, has a huge impact on the prices here in India. Gold, due to its almost steady character as compared to currency, holds significant value and is used to hedge inflation. “No wonder why investors prefer to hold gold rather than currency. Thus, as a result, when the inflation is high, the demand for gold increases and vice versa. The price of gold, then shoots up as a result of high demand from customers,” says Pavan Kumar Vijay, MD of the Delhi-based Corporate Professionals.

Impact on gold

What factors impact gold prices? Earlier this year a raft of concerns kept gold prices afloat, factors like uncertainty over US sanctions or concerns about US-China trade tariffs or the Middle East conflict. Gold usually tends to gain in times of uncertainty in the macro-environment. In the past 12 months, multiple macro-economic variables worked in favour of prices of this precious metal, some of which are: political tensions in the Middle East, worsening geopolitical tensions between US and Iran had effects on energy markets and hence on global economies. Following the news of an Iraqi commander and Iranian chief being reportedly killed in a US airstrike, spot international buyers started purchasing gold in bulk, which led to prices soaring to new highs at the beginning of the year.

Well, the yellow metal has had a fantastic run in the past 18 months – all through investment demand. “First it was the US-China trade relation. Due to uncertainties surrounding the cross-border relation between the two countries, the safe haven demand began to rise,” observes Naveen Mathur, director, commodities and currencies, Anand Rathi Shares and Stock Brokers.

The rising protectionist measures in the form of trade barriers created tensions between world’s two large economies – the US and China. Two years ago, this escalated to severe trade wars and has still not shown any signs of reaching common grounds. In fact, it has worsened now with other nations also being involved.

Gold tends to attract investors in a falling interest rate climate. Consistent rate cuts by the US Fed in 2019 and another sharp cut in March 2020 – by almost 150 bps – led to US yields falling to all time low and gave way to demand for gold as the preferred asset class of investment. “Later, People’s Bank of China started buying gold as a reserve policy to protect itself from uncertain trade relations. Brexit was a political risk the world was facing and investors flocked to safe haven assets like gold. H1CY20 will be remembered due to the spread of Corona virus from China to all over the world. In an unprecedented event, strict lockdowns in almost everywhere on the earth, the recession got triggered in the EU and Japan,” says Mathur.

According to Satish Kumar, head of equities, Equirus Securities, “The rise in gold prices always happens because of two basic reason: debasement of currency or risk of currency debasement – in this case it is US dollar and the perceived risk of inflation.” Few months back the debasement of US dollar was the biggest risk as Yuan and Euro were surging as percent of global reserves. However, since Covid-19 the perceived safety in Yuan has gone for a toss. “Having said that inflation is the biggest worry now and that will propel gold. We also need to keep in mind that enhanced risk perception also increases gold price as it has remained as a store of value for centuries,” says Kumar.

The global outbreak of Covid-19 has brought most large economies to an almost standstill. With lockdowns imposed in most nations, economic activity is severely impacted and affected global commodities and financial markets, along with earnings of firms. “Limited signs of stoppage of spread of Covid-19 have created worries and uncertainty for the myopic future. In an uncertain world, amidst the ‘3 Fs’ –Fear, Falling interest rates and Fallout of potential Covid relapse, investors are going to prefer gold, silver and precious metals,” says Sriram Krishnan, head of securities, Deutsche Bank India. He points out that gold, which has a special cultural value in Indian families, has delivered solid returns too. During the global financial crisis in 2008 gold yielded up to 24.58 per cent return while the Sensex crashed 38 per cent.

In every historical period, possession of gold remained a key indicator of a person’s economic status. But the nature of investments in gold has undergone a sea change in the present era. Especially in the last two decades, the advent of technology and rapid globalisation has brought about significant changes in investor behaviour and expectations. Millennial investors (born between 1980 and 2000), have a different approach, when it comes to taking investment decisions, be it stocks, securities, real estate or gold.

Globally, India is among the biggest consumers of gold. The liberalisation of the economy post-1990s coupled with the rise in purchasing power resulted in an increased demand of the precious metal. According to reports of the World Gold Council (WGC), out of every six ounces of gold being purchased globally, Indian consumers account for more than one portion. Wedding purchases account for around 50 per cent of the total consumer spending of gold, and gold jewellery is preferred as a safe and secure mode of investment, largely in rural areas.

ETFs, a preferred mode

Over the years, millennials have invested in various forms of gold, including physical and paperless gold. While paperless gold, like gold-backed Exchange-traded Funds (ETFs), have become popular modes of gold investments, there is a marked decline in the number of millennials opting for investment in physical gold.

The first gold ETF was launched in India in 2007. Initially, it was just before the financial crisis (Lehman), so it was slow. But demand ebbed away for three key reasons. First, India has a huge cultural affinity for gold but interest has traditionally centred on physical gold so the concept of a gold ETF was very new. Second, gold as an asset class fell out of favour since 2013, particularly as equity markets were rising at that time. And third, the government introduced sovereign gold bonds in 2015. “These eight-year bonds offer very little liquidity but they pay annual interest and, if the gold price rises, capital gains are tax free,” observes Sandeep Tandon, chief thought officer & CIO, Quant Mutual Fund.

But ETFs have now picked up. There has been almost Rs2,000 crore new buying in gold ETFs and almost Rs3,200 crore (6.73 tonne approximately) in Indian gold sovereign bonds. Consumers have started focusing more on investment rather than consumption because it’s an easy liquidity option. Hence, consumers are looking at investments through ETFs and sovereign bonds as options. “These are easily bought or sold at the stock exchange, so there may not be any liquidity issue. Also, there are no other taxes on purchasing of bonds, which we need to be paid at the time of purchasing physical gold. So, from a consumer’s perspective for the investment purpose, gold-backed ETFs is a much better option,” suggests Kothari, chief of IBJA.

“During the lockdown, investors flocked to gold ETFs, gold bonds and digital gold because these were the only avenues in the absence of physical markets. Of this, the largest beneficiary was gold ETFs which attracted a larger investment,” adds Ketan of Augmont.

Gold-backed ETFs are listed and traded on the National Stock Exchange of India (NSE) and BSE Limited. “Yes, ETFs have attracted huge inflows of late. It is tax-efficient, gold purity in these funds claims to be backed by gold with 99.5 per cent purity, investors can purchase as low as 1 unit, i.e. 1 gram, no fear of loss or theft as held in an electronic form and no premium or making charges,” reasons Ankit Agarwal, MD, Alankit Ltd.

“We have seen an increase in the AUM of gold ETFs in the past 12 months from Rs4,894 crore in June 2019 to Rs10,099 crore which is a rise of 106 per cent. We are of the view that gold ETFs are a better option to invest in gold as it comes with the advantages of safety, convenience and liquidity,” observes Himanshu Kohli, MD of the Delhi-based Client Associates, which does wealth management business.

Due to the pandemic, the safe-haven demand for gold has increased and is reflected in inflows into gold ETFs recently. “The current situation is unprecedented as movement of physical gold has been severely restricted due to lockdown, therefore demand was channelised into ETFs. Whether this continues once lockdown eases and jewellery stores are fully functional is an open question. KYC and compliance requirements differ widely between ETFs and jewellery trade, and for this reason, gold buying through jewellery trade will always be the preferred mode,” says Somasundaram of WGC.

However, the recent activity in gold ETFs highlights the positive role organised financial channels can play in promoting transparent gold investments, when situation normalises. “Allowing bullion banking in India and promoting a spot exchange will transform gold investment scenario and make gold a part of mainstream financial savings,” adds Somasundaram.

Geological tensions

“Uncertainty surrounding the economic impact of Covid-19, geopolitical tensions and central bank purchases continued to drive inflows into gold highlighting the increasing acceptance of gold ETFs among investors as a means to gain exposure to gold,” says Sriram Iyer, senior research analyst at Reliance Securities pointing that, according to World Gold Council, central bank net purchases totalled 39.8 tonne in May, in line with net purchases in March and April, and above the monthly average of 35 tonne over the first four months of this year. “We continue to see improved flows into the gold ETFs in the next 6 months to 1 year,” adds Iyer.

Concurs Ravindra Rao, VP-head, commodity research, Kotak Securities, ETF inflows has been the major supporting factor for gold this year. Gold holdings with Standard & Poor’s Depositary Receipt (SPDR) ETF, the largest gold backed fund, was last reported at 1,182.113 tonnes, the highest since April 2013. In 2020, so far (till 1 July), the fund has seen an inflow of about 280 tonnes as against an inflow of about 105 tonnes in the entire year of 2019. “ETF investors may continue to hold on to the metal until they see risks to the global economy and this may continue to support prices.”

Gold savings

Most large fund houses, offer Gold Saving Plans (GSPs). Through the GSP, it is easy for investors to start systematic investment plans (SIPs). GSP invests in gold ETF so investors can either invest in the Gold ETF or the Gold Savings Plan, depending on their preference and comfort levels. It’s generally easier to implement a SIP strategy in a traditional mutual fund format like a GSP. Investors can approach asset management firms directly to set up a plan and they are provided with a single end-of-day valuation too.

Indians are known to have a strong affinity towards gold, traditionally considered to be a store of value and a wealth preserver. “Purchasing gold in the form of jewellery, bars or coins is considered as a ritual in Indian families. Almost 75 per cent of the households in India purchase gold occasionally, while the financially stable income groups purchase the yellow metal more frequently,” says Sachdeva of Religare Broking.

So where do analysts guess the trend is? Sachdeva says, “Gold prices have witnessed a steep rally of 12.9 per cent in the second quarter of 2020, their highest quarterly gains in four years. However, from an immediate short-term perspective prices are expected to remain capped around $1,800 per ounce and witness some correction as various countries reopen and economic activity starts to pick up, which has raised hopes for recovery. Positive set of economic data from the US and China have also fuelled risk-on sentiments in the market. This can dent the demand for safe haven asset-gold to a certain extent.”

“Global debt has exploded over the last three decades since the Plaza Accord (1985) and unleashing of the Reagonomics premised on debt funding of government deficits and more so in the form and nature of Quantitative Easing since the financial crisis years 2008-09. The total amount of government debt globally is now estimated to exceed $220 trillion, more than three times the world GDP, according to the World Bank and other international research agencies. The G7 advanced economies’ debt is higher than it was post WW-II. Including pensions and other unfunded liabilities, the world now is deep in the debt trap,” says Suresh Jain, MD, Sun Capital, pointing out that much of the new debt since the financial crisis (2008-09) has been accumulated by the three largest economies – US, China and Japan.

“The situation, in other words, is different this time – it’s much worse. Because, debt has undoubtedly remained an essential tool for financing economic growth, the panacea, politicians believe but do little, to remove or reduce the wealth and income inequality. The attempt to solve what was a global debt crisis with mountains of more debt means we might have another global financial crisis – the question being when rather than if,” adds Jain. Certainly, this will have an impact on illusory economic recovery and on asset prices that will necessitate diversification which must include allocation for gold, the real hard asset and real money; money of the last resort.

ETFs globally have gained steam as large investments are in these funds which can be converted to gold any time by investors. “Hence they have the security of not needing to hold on to the asset while deriving the benefits of the same. This has been the main reason or the demand push for the metal which has driven the price up. Also central banks’ demand should be going up with a weaker dollar,” says Sabnavis.

“Hefty inflows have been seen in North America and European Gold ETFs given the escalating economic uncertainty and ensuing risk aversion. Global ETF holdings are around 3,191 tonnes from 2,582 tonnes the beginning of this calendar year. Similarly, World’s largest ETF SPDR Gold has seen its holdings rise to 1,178 tonnes from 893 tonnes at the beginning of this year,” points out Hitesh Jain, lead analyst – institutional equities, Yes Securities.

Precisely, reflecting investor appetite, the world’s largest and the most liquid gold ETF is SPDR Gold ETF, it has attracted a significant amount of inflow in 2019 and this year also. From 795 tonnes as on 1 January 2019, it has gone up to 1,191 tonnes in 3 July 2020. “The highest since April 2013 – the rise in the investment demand signifies that the investors are concerned regarding global growth, recession, the trade relation between the US-China. We believe, going ahead, since political risk is also a major driver of investment demand, the ETFs will have a comfortable rally in coming months,” says Mathur of Anand Rathi Shares and Stock Brokers.

There has been a strong investment demand for gold this year which is reflected by the huge inflows witnessed in global gold-backed ETFs. “A phase of continuing growth streak is quite palpable. In spite of the fact that physical demand from India and China, the traditional retail buyers has remained very tepid due to lockdowns, demand in the form of gold ETFs especially by the western investors who are seeking safety from the virus induced slowdown has remained quite robust,” says Sugandha Sachdeva, VP-Metals, Energy & Currency Research, Religare Broking, recommending that, with expectation of deep recession engulfing the global economy, gold as an asset class is likely to witness steady investment demand in ETFs for the rest of the year as well.

Demand from millennials

Wealth managers across the globe and in India are advocating exposure to gold investment products and there is a particular interest from high net worth and ultra-high net worth individuals. Even the millennials are drawn to the market as well, seeing ETFs as a smart way of investing in gold rather than buying physical gold. “Essentially, it is in times of stress that people recognise the value that gold can bring to a portfolio. India has a centuries-long affinity with physical gold,” observes Tandon.

As a country, we import around 800 tonnes of gold a year, accounting for approximately 25 per cent of global demand. In other parts of the world, such as the US, investment products account for 80-90 per cent of demand for gold. “In India, it’s the reverse and that will take time to change. But I think it will change. There are lots of issues around physical gold. Purity is hard to gauge, different vendors offer different prices, storage can be a challenge and people are often disappointed at the price they are offered when they come to sell their gold,” adds Tandon, “looking ahead, the outlook for gold ETFs seems promising”.

Policy-makers can drive the rising appeal of gold investment products, such as ETFs. India has two levels of capital gains tax, Short-Term Capital Gains (STCG) and Long-Term Capital Gains (LTCG). The higher levy applies to assets held for three years or less. The lower level applies to assets held for more than three years. “At the moment, gold ETFs are subject to the three-year rule. A tax benefit to listed, gold-linked products could lure investors away from physical gold. LTCG for listed, gold-linked ETFs could be reduced to one year as an incentive. This would reduce demand for physical gold thereby reducing India’s dependence on gold imports,” suggests Iyer.

Currently on tap is the subscription for the fourth tranche of the Sovereign Gold Bonds (SGBs) scheme, the 2020-21 Series IV is open for subscription and will close on 10 July, 2020. The SGBs will be allotted on 14 July. “This is a great opportunity for you to invest in gold. SGBs are government securities denominated in grams of gold. These are substitutes for holding physical gold. SGBs are issued by the central bank on behalf of the Government of India. Investors have to pay the issue price in cash and the bonds are redeemed in cash on maturity,” says a Sharekhan newsletter. It lists out reasons: the yellow metal acts as a hedge against inflation; it is a relatively stable investment compared with equities; it is a good diversification strategy; and it can be purchased easily.

Salient features of the current SGBs – it carries a fixed interest rate of 2.50 per cent per annum on the amount of the initial investment and the interest is credited semi-annually to the bank account of the investor. “SGB prices are linked to the price of gold of 999 purity published by India Bullion & Jewellers Association (IBJA). Investing in SGBs eliminates the risk of theft and the cost of storage. Investors are assured of the market value of gold at the time of maturity and periodical interest. SGBs are free from issues like making charges and purity associated with purchase of gold in jewellery form. These bonds are tradable on the exchanges.

SGBs have a tenure of eight years and early encashment/redemption of the bonds is allowed after the fifth year. Interest on SGBs is taxable but the capital gains tax arising on redemption of the bonds is exempted for individuals. SGBs can be used as collateral for loans. SGBs carry the sovereign guarantee as these are issued by the RBI on behalf of the Government of India. The government opens the window for sale of SGBs, once in every two-three months. One can also purchase earlier issued SGBs – any time you want – at market value listed in the secondary market.

Concern over pandemic

Nonetheless, the pandemic has yet not been contained. The second wave of pandemic is yet to unfold its consequences, which according to the WHO could be more dangerous than the current one. “Considering the backdrop, the precious metal looks primed to test levels of around $1,900 per ounce by year end and $2,000 per ounce by Q1 2021, after a brief period of consolidation,” cautions Sachdeva .

“The gold prices respond sensitively towards crisis, uncertainty and economic upheaval in markets. They could touch Rs65,000-Rs68,000 over next 12-24 months, but it would depend on the movement of rupee versus the US dollar. In my opinion in two years is a longer period, the record could be broken in one year only. Even after the Covid-19 pandemic recedes, gold may continue to log stellar returns. Covid-19 impact could take longer for economies to recover, and easy monetary policy is here to stay for at least two years, and this will continue to promote gold,” says Pavan of Corporate Professionals.

One most major issue that remains is that the future is still bleak. The vaccine against the root cause has still not been developed. Moreover, even if we find the vaccine today itself, the situation will not heal completely in the short term. Also, with many businesses, start-ups and even the unicorns have been crushed under the crisis.

It is wise to understand that there will still be problems to tackle with and the time to stand up again will still take a little longer than expected. It will take time even when the remedy is discovered. So, considering the gravity of the situation, it is highly likely that the gold price will continue to rise towards all-time highs over the next two years.

Most analysts Business India spoke to are of the opinion that, as the global economic landscape looks edgy due to the Covid-19 pandemic, gold as an asset class is likely to invite a lot of attention and entice buying interest due to its safe haven appeal. Barring intermittent corrective phases, prices look to traverse further on the upwards trajectory and even breach record highs marked in 2011.

“As economies reopen and the world emerges from the Covid-19 crisis, some correction in gold prices cannot be ruled out, but the environment of low interest rates, rampant monetary stimulus by the major central banks, geopolitical risks and simmering US-China tensions will keep the spotlight on gold.”

Also, if one were to draw an analogy to 2008-09 financial crisis and steep rise in gold during the subsequent years, it further reinforces the view that the yellow metal is inclined to tread higher and witness a sustained and prolonged rally over the coming years.

Meanwhile, the trade war between the US and China is far from over. It is hard to imagine that either of the two will back down immediately which suggests that this dispute will continue. A trade war could affect demand for US assets just as the budget deficit swells, leaving the dollar vulnerable should international buyers shun US debt.

The aggregate federal, state and local debt in the US, both on balance sheet and entitlements, relative to levels of savings and investments in the economy, will contribute to worries over the longer term purchasing power of the dollar, particularly in view of low current yields. Should there be a “deep trade war”, with complications for global growth, industrial commodities such as base metals, energy will be negatively affected, but that scenario would benefit gold.

When everything else fails in this money maelstrom, gold has been and will be money of the last resort.

A golden dawn

Through Quant Global Research’s (qGR), a product of Quant Mutual Fund’s predictive analytics, it is observed a Volatility Expansion Phase (VEP) between 2018-2023 and gold remains to be one of the preferred asset classes in this environment of elevated volatility. After forming a peak in September 2011 at $1,921, it is observed a correction and consolidation in gold. Finally, we witnessed a breakout in June 2019 and since then; it remains to be a consistent performer.

“Based on qGR’s Cycle Analytics, from a long-term cycles standpoint: gold is showcasing massive strength in comparison to any other metal (both precious and base metals). Based on the spike in PVIX (Political Volatility Index), we can justify the consequent rising geopolitical volatility. In scenarios of heightened political uncertainty, it has been observed that gold is picked as the preferred asset class. According to qGR’s Cycles Analytics, 2020 will remain to be a constructive year for gold as compared to the past years, says Sandeep Tandon, chief thought officer & CIO of quant Mutual Fund.

Though gold is generally considered as an inflation hedge, the large gold price rally from 2001 to 2011 happened during a deflationary period. qGR’s Cycles Analytics suggests that the rally which started from $255 in April 2001 and lasted until September 2011, is actually just the first phase of a multi-stage bull run for bullion and qGR believes that global inflation will start inching up from the second half of 2021. This will further support gold prices from a long-term perspective.

In the VEP between 2018-23, qGR doesn’t expect a linear movement in gold. During this hyper-volatile phase, a possibility of steep corrections of $200-300 prevails in the asset class. qGR’s Cycles Analytics anticipates gold to be a consistent performer in the final phase of volatility expansion (around 2023). Subsequently, gold will start its multi-decade rally beginning late 2024 or early 2025. qGR’s Cycles Analytics endorses that by 2050 Indian households will emerge as one of the wealthiest globally owing to their possession of sizable physical gold.

“A substantial increase in the prevalence of crypto currencies and usage of gold-backed crypto currencies is the future. Combining the innovation of blockchain technology with the history of gold as a store of value can have vast economic and geopolitical ramifications.”

Several such crypto currencies already exist, notably the OneGram project of UAE, Singapore’s regulated Puregold Token and Digix Gold Tokens and other popular gold surrogates around the globe. What’s caught our eye are the plans laid down by the central banks of Iran and Russia to launch gold-backed crypto currencies to circumvent sanctions and offer a stable alternate to their volatile fiat currencies. “The success of these gold-backed sovereign crypto currencies can further support our predicted gold rally by increasing access and liquidity, while also accelerating the demise of the USD-led global currency system,” sums up Tandon.