-

It is a matter of choice for Tatas on how to pay the consideration

Shailesh V Haribhakti; Photo: Sanjay Borade

Separation vs buying of shares – applicability of quasi-partnership principles

Both sides have now publicly made known their intention to end the vexatious relationship lasting several decades. “Once there is clarity from the courts and clarity of intent from both sides, which I believe is there, the issue becomes simpler,” says Shailesh V Haribhakti, chairman Haribhakti & Associates. An astute corporate watcher, Haribhakti adds: “Determining the value of the shares may take a few weeks or months, but once it is done, it is a matter of choice for Tatas on how to pay the consideration.”

SP group has stated before the Supreme Court that a separation from the Tata group was necessary due to the potential impact this continuing litigation could have on livelihoods and the economy. It had stated that “it was crucial that an early resolution is reached to arrive at a fair and equitable solution reflecting the value of underlying tangible and intangible assets”.

By asking for a separation, SP group is asking for an asset separation of all assets, including the brand value of Tatas’ underlying shares in all operating companies, listed and otherwise. Before taking up the question of how the valuation has to be determined by the parties, the issue which may crop up before the court is the tenability of whether the exit can be deemed to be a separation or not.

Normally, an asset separation is done in a partnership firm. In rare cases, the principles of a quasi-partnership are also applied to companies by the courts. In a few instances in the past, the courts have lifted the corporate veil to apply principles of quasi-partnership to judge the true character of a company and the business realities of the situation.

While the Companies Act 2013 does not have a specific provision on quasi-partnership, under Section 242, a tribunal is given powers to end matters as it deems fit in cases where complaints have been made. This is known as the just and equitable principle. These powers include matters relating to the purchase of shares of any members of the company by other members and, in the case of purchase of its shares by the company as aforesaid, the consequent reduction of its share capital.

The courts have, in the past, held that the principles of quasi-partnership are not foreign to the concept of the Act and can be applied to even a public limited company. The plea of quasi-partnership was already upheld by the NCLAT in its judgement passed in December when it struck down Tata’s move to convert Tata Sons into a private limited company.

Lawyers are of the opinion that Mistry will try and put forth the argument that the relationship with the Tatas went far beyond being just a financial shareholder in Tata Sons. The origin of the company, viz Cyrus Investments, which was earlier known as FE Dinshaw Ltd has been associated with Tata Sons since 1927. From 2 July, the company was entitled to a two anna (1/8) share in the commission paid by operating company Tata Steel and subsequently Tata Power to Tata Sons. Shapoorji Pallonji, by virtue of being firstly a shareholder in FE Dinshaw since 1928, and thereafter a majority shareholder since 1950, also had a share of managing agency commission till 1970.

-

One earnestly hopes that it ends in a win-win situation

Raamdeo Agrawal; Photo: Sanjay Borade

SP group had inked an agreement with JRD Tata, for development of his land in Pune in 1966. It inked an agreement with Naval Tata, the father of Ratan Tata, for development of his private property in Mumbai, the Sterling theatre in South Mumbai. Forbes company was bought by the SP group from Tatas. Likewise, the Tatas bought Special Steels from the SP group. Pallonji, son of Shapoorji and his sons, Cyrus and Shapoor, enjoyed a personal bond with Tatas and were also on various boards of companies for more than five decades.

Most construction contracts of Tatas were executed by the SP group, which has over 18 large companies and has been in existence since the 1880s. Amongst the early works, the SP group lists the building of a water storage tank at Malabar hill in Mumbai for supplying water to the city of Mumbai, as being executed by one of its companies in 1888.

In the normal course of events, the courts may have to decide if the relationship of Mistry could be seen as a quasi-partnership and subsequently whether asset separation is merited or not. Settlement of disputes through asset reduction is just one possibility for ending the vexatious relationship. Others include seeking the advice of independent valuers or forming an arbitration committee or going by the mode suggested by the Supreme Court. Normally the courts leave it to the parties concerned to arrive at a fair and just valuation, but in this case, involving the largest industrial group, they may get involved.

In the interest of both sides to cut short the tortuous litigation to settle the matter within themselves. In which case courts will not be required to judge the valuation but rather give its blessings to the parties. Considerable time for litigation would be saved by arriving at a consensus between the parties.

The last time such an exercise of separation was done, it was in the case of the Ambani brothers, Anil and Mukesh. However, that was a family settlement and there was a common advisor, with Mrs Ambani, their mother, being the final arbitrator. Other family settlements are decided by the patriarch of the group. This was the case with the Birlas and RP Goenkas – all were settled within the confines of the families.

Undoubtedly, there have been acrimonious disputes in many groups and the Supreme Court has had to play a big part in such cases. And this does not only apply to cases of intestate heads of large empires. Even wills have been challenged – the case of MP Birla is the most current one.

In the case of Tatas-Mistry, however, some framework has to be put in place. Independent valuation experts, either from India or overseas, may be asked to step in. “The biggest challenge, once the stalemate ends, is to have discussions over the valuation of Tata Sons,” says Amit Tandon, MD and co-founder, Institutional Investors Advisory Services, adding “that is the only way forward”.

-

Getting funds from Sovereign Wealth Funds is one option

K. Balakrishnan; Photo: Sanjay Borade

Valuation of India’s largest group holding company

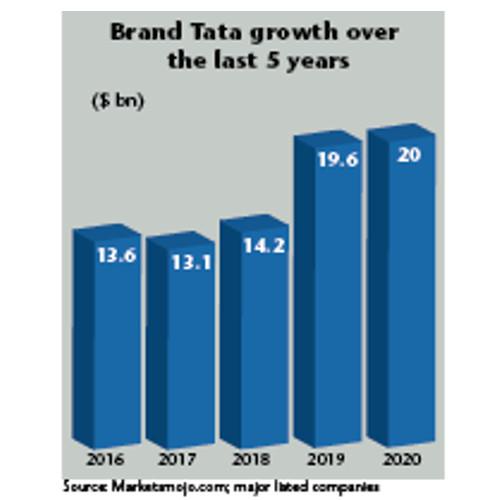

Tatas are unlikely to accept asset separation nor are they likely to agree to a consideration for the brand Tata. Brand Tata has been valued at $20 billion by an independent firm, Brand Finance India 100. This is marginally higher than the $19.6 billion estimate in 2019 but significantly higher than the $14.2 billion figure in 2018. (ee chart for brand value). Tata Sons was formed nearly 150 years ago as a partnership firm. It became a private limited firm in November 1907. FE Dinshaw was inducted as a shareholder later. Shapoorji Pallonji came even later.

In that sense, neither had built the brand, which was already in being before Tata Sons was incorporated. However, one point of view is that even preservation of goodwill counts as much as being partners since inception. On several occasions, Pallonji Mistry has helped Tatas and they can also claim active participation, with Cyrus at the helm for two years, in growing goodwill. During Cyrus Mistry’s tenure in 2014, the goodwill of the firm was valued at $21.1 billion.

Besides the brand, the valuation of the listed shares may be easy as both market value, book value and Ebitda figures are all readily available as is the shareholding of Tata Sons in each. Book value is normally used in the case of a breakup of assets and may not be relevant in this case. The largest company in the group is TCS, which is valued at a little over Rs9 lakh crore with Tatas holding 72 per cent.

Titan is the only other company with a valuation of over Rs1 lakh crore, with Tatas holdings at 53 per cent. Valuing by considering the average of the past five years or 10 years is a matter of detailing upon which parties have to agree. Unlisted companies like Tata Sky and a few others may form a small fraction of the listed companies.

One figure doing the rounds is Rs7.80 lakh crore being the value of listed shares, Rs44,000 crore for unlisted shares and Rs1.46 lakh crore for the brand value, all totalling to Rs9.70 lakh crore. The value of the SP group based on this calculation amounts to Rs1.78 lakh crore.

Tatas have reportedly scoffed at this figure, which is but natural. In any settlement, the sellers will try to seek the highest price for their shares while the buyer will look at getting the shares at a bargain rate. A settlement is normally reached at a rate somewhere between that put forth by buyers and sellers depending on bargaining powers and the ability to continue bargaining. SP group requires some immediate infusion of funds in their group companies, which have been impacted during the pandemic.

Another point which is likely to crop up during the settlement is the holding company’s discount, which varies between 20 per cent and 40 per cent and even more in some cases. Especially as Tata Sons is an unlisted company. Says Raamdeo Agrawal: “Both sides are mature enough to see the difference between a break-up value and the market value which may often be in multiples of 10x if not more.”

-

The biggest challenge now is the valuation of the shares of Tata Sons

Amit Tandon

The valuation will in any case be circumscribed by what the price Mistry may get otherwise. Tatas have the rights of first refusal but in case they refuse and allow Mistry to sell it to any third party, it will possibly not fetch the same price as it being offered by Tatas. Commercial prudence will require both side to strike a fair deal.

Tatas, according to some, will try to arrive at a settlement before the end of the year. The Super app being developed by Tata Sons is still a work in progress and may be launched sometime in 2021. A delay in arriving at a settlement price could possibly see the Shapoorji Pallonji group laying claims on the value of that app too. If the app is launched through TCS or a subsidiary of TCS, the market cap of TCS will go up significantly. Some say it could be more than the current value of TCS itself.

Raising funds

Once a settlement over the value of SP group’s holdings in Tata Sons is reached, the next problem will be on the payment front. Even for the 150-year-old house of Tatas, it may be difficult to pay the entire sum in one lot. They may have to seek outside funds, be they from sovereign funds or endowment funds like Harvard or Stanford University.

Ajay Garg, founder of Equirus Capital, a full-service financial company, says: “Investors will be happy to invest in Tatas. It has scale and it has reasonable growth prospects. They will look at it as an opportunity to play on the growth in the Indian economy.” A view shared by Sailesh Haribhakti who says: “Tata is a well-respected group globally; raising funds will not be a big challenge. They will be able to do it in multiple ways.” Not everyone is so optimistic on the ability of Tata Sons to raise funds.

Kavil Ramachandran, professor & executive director, Thomas Schmidheiny Centre for Family Enterprise, Indian School of Business, says: “Raising around $20 billion is not easy despite the huge liquidity in global markets. Sovereign funds or pension funds with a long-term horizon may invest. However, these funds also look for growth.”

Says K Balakrishnan, founder, Kriscore Financial Advisors, a cross border M&A Advisory firm: “Getting funds from Sovereign Wealth Funds, (SWF), may be one option. Tatas is a well-respected name overseas and the Singapore government or SWF in the Gulf countries may look at taking long term bets.” Balakrishnan, who earlier headed Lazard India’s operations, was instrumental in getting the Tata-Docomo deal earlier candidly points out: “It is not easy as even pension funds and long-term funds may look at annual yields of 5-6 per cent. They are sure to put in funds with covenants attached. Tatas could also look at the restructuring and sale of some of its loss-making companies.” He is, however, confident that Tatas will be able to seal the deal.

-

Reliance Industries has shown the way of how strategic investors can be roped in the operational companies

Deven Choksey; Photo: Sanjay Borade

There is certainly no dearth of funds, globally. Sovereign Wealth Funds from Norway, Abu Dhabi, Saudi Arabia and Kuwait are more than adequate to fund Tatas. The Singapore government’s two investment arms, Temasek and Singapore Investment Corporation, together have more than $300 billion. However, it may be challenging for a single SWF to take on a large exposure. It could well be that several SWFs with a few endowment funds could take a stake. Endowment funds, pension funds or sovereign funds may, however, put certain conditions ahead of parting with funds.

A good thing for Tatas is that the global markets are awash with funds with interest rates in many countries yielding near negative returns. In many cases, safety overrides the returns aspect. Tatas will have to seek funds and ensure that conditions put by the funds are not too restrictive and do not impact its freedom in running the operating companies of the group.

Taking debt is an option as servicing loans at even 4 per cent interest will be a challenge. The total net profit of the listed companies of the Tata group has been estimated at Rs25,046 crore by Marketsmojo.com.

As much as an amount of Rs31,217 crore is already used for funding the losses of some companies in the group. And profits for Tata Sons, are dependent on the dividends from operating companies. If the few hundred crore are used for servicing debts it will leave that much less for Tata Trusts’ charitable activities.

Getting growth capital is also important

One view is that Tatas need to raise funds not just to settle with Mistry but also raise growth capital. Deven Choksey, MD and founder of KR Choksey Financial Services, a research based broking house says: “I foresee the entry of both financial investors at the holding company level as also strategic investors in operational companies. Money should be got in not just to repay obligations but also to scale up growth exponentially. Reliance Industries has shown how strategic investors can be roped in operational companies. Sovereign funds, pension funds with 20-25 years’ horizon should be easy to get.”

Tatas should settle the dispute expeditiously and become future ready

Getting funds in a holding company may not be so easy, unless the structure of Tata Sons is overhauled. Investors, whether SWF or others – everyone looks for exits. With the government of India frowning on structured buy-back deals it becomes even more difficult. Amit Tandon says: “The structure of Tata Trusts and Tata Sons was created in an earlier era when times were different. A rethink of the holding structure appropriate for the time is the need of the hour.”

-

Raising around $20 bn is not easy despite the huge liquidity in global markets

Kavil Ramachandran

Like in any large conglomerate, not all companies in the Tata group are doing well. A few require to be nurtured for some more time. Especially those in cyclical industries like steel and auto. For a 150-year-old house which has the potential to carry on for another 150 years, solutions have to be found from within the group. And the necessary structures which take a holistic view will emerge in due course.

For now, the attention of the group is on launching the Super app, an app which could offer retail solutions to over one million of its customers across companies. A lot of work has gone into building this app and once launched it could become a real game changer, just like the Jio and retail verticals have done for Reliance Industries.

Given TCS’s wide exposure to technology and computing prowess, it may well make sense for Tatas to get into medical science. Tatas should have a judicious mix of old economy, new economy and future assets to make it a truly future ready group.

The immediate task at hand for Tatas is to ensure an expeditious settlement and bring a close to the Mistry episode. This will give it more breathing space and allow it to direct its energies towards its existing companies and the ones being built in the new age sectors. Whether Cyrus Mistry and Shapoor Mistry manage to be in the top 10 list of the India’s wealthiest people should be no concern to any one but the Mistrys.

The huge liquidity will also attract several investors, with whom they could strike lasting alliances. It will give them a golden opportunity to script a new chapter in the annal of the 150 year old group. Tatas have a lot of work besides settling the dispute with Mistrys and carry on with absolute majority in Tata Sons.

-

What can $20 bn buy?

$20 billion is a huge amount. A few billions here or there cannot make much of a difference. Currently, the Mistrys may not be looking at what the wealth could buy, once they have it. Maybe a billion-and-a-half could be used to fund the immediate requirements of their operating companies.

They can go company shopping in India or the UK or any place they feel like. If they want to ride the India story, they could look at buying majority stakes in banks in India; Axis Bank, where the promoters’ stake is shown as less than 15 per cent, or even strike an alliance with L&T whose market cap is Rs1.42 lakh crore. If they feel that the US is the country to watch out for, they could look at buying reasonably big stakes in Citigroup or GE, the bellwether stocks of USA, which are available at bargain rates.

If they feel that building portfolios is a mug’s game, they could get into buying iconic buildings. Mistry could well become the biggest buyer of commercial land and property in India. The property market during the pandemic is undergoing a drastic change, especially commercial property where aggregators have to deal with vacancies in a big way with more and more IT companies embracing work from home and vacating large premises.

If they want to create iconic buildings themselves, like they have done in the past, they may well opt to buy chunks of property and build eye-popping towers which could well become tourist attractions. If they zero in on Gujarat, GIFT City has a lot of potential. Or they may choose to build one more GIFT city in Delhi or Mumbai.

A super private equity company like Blackstone could be looked at. Blackstone itself must be stuck with huge properties, with IT tenants in many not looking at renewal of leases.

If they wish to take a break from building mansions for others, they could, just for the heck of it, do what Topol in Fiddler on the Roof, dreamt of: a big tall house…. with one long staircase going just up and one more leading nowhere – just for show!