-

It is only a matter of time before we see increased application of AI /ML for banking use cases, like the effective and early detection of frauds

Jaya Vaidhyanathan, CEO, BCT Digital

New developments, newer frontiers

With the latest introduction of account aggregators, API readiness of banks and NBFCs, and the launch of many neo-banks, the future looks promising for the Indian fintech space. Indians have already embraced the power of open banking and are likely to adapt to new technologies with ease. As the industry continues to evolve, technologies such as AI, IoT, cloud computing, quantum computing, and blockchain are expected to change the nature of financial services and the ways they are offered.

Indeed, the impact of fintech on the Indian economy cannot be overstated. “Fintech has had a significant impact on the Indian economy and in the Indian banking sector. Fintech has enabled banks to offer digital banking services to customers, reducing the need for physical visits to bank branches and leading to cost savings for both banks and customers. At Capital Small Finance Bank, we focus on delivering a seamless integrated solution to ensure a consistent, high level customer experience through branch banking, mobile application, website, and internet banking. This allows faster and more profitable operations, while maintaining consistency in services. Fintech has also facilitated the growth of digital payments and alternative lending platforms, leading to increased entrepreneurship and job creation in the economy,” says Sarvjit Singh Samra, MD and CEO, Capital Small Finance Bank.

Little surprise, then, that India has emerged as the world's third-largest fintech market, trailing only the United States and China. Over the past 5 years, more than 1,000 fintech companies have secured funding and attracted over $15 billion in investments. With a vast, underpenetrated market and favourable demographics, India's fintech landscape is ripe for innovation across product offerings and delivery channels.

Abhishant Pant, founder of The Fintech Meetup, believes that the sector’s growth is just beginning. He envisions a deepening collaboration between traditional financial institutions and fintech companies, which can drive financial inclusion in India and bolster the nation’s economy. “As more individuals and small and medium-sized enterprises become part of the formal financial ecosystem, fintech companies are poised to become primary drivers of this formalisation,” he explains.

All this has made fintech a crucial enabler and a significant catalyst for India's GDP growth. By introducing novel business models, enhancing efficiency, and promoting financial inclusion, the digital revolution within the financial services sector is unlocking economic potential. Fintech companies, through their inventive solutions, are bridging the gap between the underserved population and formal financial services, thereby contributing to the nation's overall economic growth.

The ripple effect of increased access to credit and financial services provided by fintech firms extends to other sectors like manufacturing and infrastructure, which are crucial for GDP growth. Jinand Shah, MD & CEO of Online PSB Loans, highlights the role of fintech in supporting the Indian economy:

“Our contribution to the economy is facilitating increased credit access for Indian MSMEs and eliminating the stigma associated with credit. A robust credit system is the foundation of a stable economic system. Currently, MSMEs in India contribute to almost 30 per cent of the country’s GDP, and this percentage can only be improved through the combined efforts of fintech companies, banks, and regulators.”

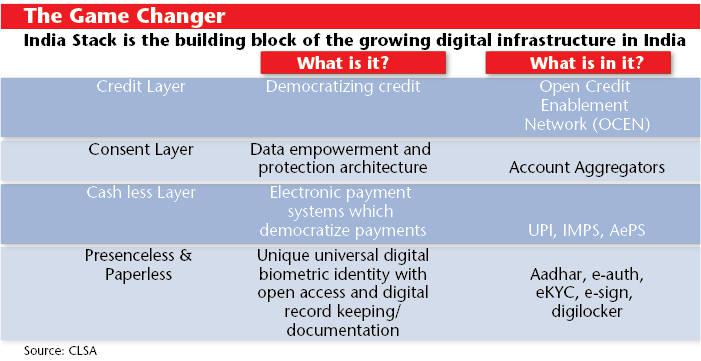

The pioneering India stack

India's fintech scene is further bolstered by the unique open digital infrastructure known as India Stack. Developed through a collaboration of government and industry bodies, this trailblazing platform serves as the foundation for the nation's rapid fintech evolution. Touted as the world's largest open API, India Stack has empowered stakeholders to leverage an open digital infrastructure and has become the cornerstone of India's fast-paced fintech transformation.

-

India Stack has been implemented in stages, with the first step being the introduction of the Aadhaar Universal ID numbers in 2009. These unique IDs are linked to biometrics, such as fingerprints, and provide users with access to various services and subsidies. However, this has raised concerns about privacy and surveillance, particularly given that the users’ interface with the system is primarily via their mobile phones.

The subsequent stages of India Stack have included the introduction of eKYC (electronic Know Your Customer), which facilitates paperless and swift verification of identity, address, and other relevant details. This was followed by e-Sign, which allows users to attach legally valid electronic signatures to documents, and UPI (Unified Payments Interface), which enables cashless payments. The most recent addition to India Stack is DigiLocker, a platform for issuing and verifying documents and certificates.

Since the deployment of India Stack, India has been organising hackathons to develop applications for the APIs. This has created an environment of innovation and collaboration, where fintech companies are able to leverage India Stack's open infrastructure to develop new and exciting products for their customers.

However, India Stack's implementation has not been without its challenges. The increasing reliance on Aadhaar authentication for accessing services has raised concerns about data privacy and surveillance, and there have been legal challenges to the constitutionality of Aadhaar. Nevertheless, the potential benefits of India Stack – such as rapid financial inclusion and payment digitization – cannot be ignored.

As the fintech landscape continues to expand in India, with segments such as payments, insurtech, neo banks, digital lenders, and wealth-tech, India Stack's open infrastructure has become an essential tool for companies looking to create niche products for their target audiences. It is an exciting time for the Indian fintech industry, and India Stack is leading the charge towards a more inclusive, digitised financial ecosystem.

The first two layers of the India Stack, biometric digital ID (Aadhaar) and UPI, have already brought about rapid financial inclusion and payment digitisation. With these secure and reliable tools in place, people from all walks of life can access banking and financial services, including those in remote areas where traditional banking infrastructure is lacking.

The development of India Stack is now going to the next level. The next two layers, safe data-sharing account aggregators (AA) and the open credit enablement network (OCEN), are expected to further democratise lending and propel the fintech space forward. These tools will allow for seamless and secure sharing of financial data, making it easier for lenders to evaluate creditworthiness and extend loans to a wider section of society.

In fact, the Indian government has long recognised the importance of financial inclusion as a means to drive economic growth and reduce poverty. Besides, the government has launched a number of initiatives aimed at bringing financial services to the underserved and unbanked population. These initiatives, including the Pradhan Mantri Jan Dhan Yojana (PMJDY) scheme, have been a boon for the fintech industry in India, as they have created a vast pool of potential customers who are looking for affordable and accessible financial services.

-

The next advancement in adoption of digital transformation will evolve from digitisation of customer touchpoints to digitisation across the entire organisation

V Srinivasan, Executive chairman, eMudhra

Additionally, the supportive demographics of India have also played a role in the growth of the fintech industry. Further, the availability of low-cost data and increased affordability as income grows have contributed significantly to the rise of internet and mobile usage in India. As a result, there has been a surge in internet penetration, exponentially narrowing the gap between telephone subscribers and internet users.

In fact, the internet user base has expanded from 0.52 billion to about 0.85 billion in just 4 years (2018-2021). By FY25, the number of active internet users is expected to reach 0.95-1 billion, indicating an enormous market for fintech in India.

Another reason behind the meteoric rise of fintech in India is the high penetration of internet and mobile usage, which is similar to that of China. India has also seen the unprecedented transformation in its financial landscape, thanks to a trinity of revolutionary concepts – Jan Dhan, Aadhaar, and Mobile, commonly known as the JAM trinity. This innovation has resulted in the country's growth from one of the world's most unbanked economies to one where most adults have bank accounts.

This remarkable achievement has not been realised by many developed economies yet. Jaya Vaidhyanathan, CEO, BCT Digital, believes the critical component behind this transformation is 4G mobile telephony. It has made the internet accessible to every section of society at a low cost, bypassing the conventional trajectory of fixed line and broadband services.

In her words: “This is the single largest innovation that has been shaping Fintech.” The JAM trinity has opened the door to fintech start-ups, allowing them to develop innovative and differentiated business models in the world's second-most populous country. This has positioned India as the next big market for the fintech industry, with immense potential for growth.

In addition, the introduction of Aadhar (as a means of fulfilling ‘know your customer’ norms) has also played a significant role in enabling fintech solutions. The unique identification number, Aadhar, linked to biometrics, has allowed for paperless and rapid verification of identity, address, and other important details. This has reduced the time and costs associated with manual verification processes and enabled greater financial inclusion by bringing more people into the formal banking system. With fintech companies leveraging Aadhar and other digital records to offer innovative and affordable financial solutions, the sector is expected to continue to grow and drive economic development in India.

“The four main offerings of UIDAI’s Aadhaar – e-authorisation, e-KYC, e-sign and DigiLocker – have simplified customers’ ability to verify identity, furnish details digitally and save electronic copies of important documents in cloud storage. The Aadhaar card is far ahead of peers from developed countries, such as the US Social Security Network (US SSN) or the UK National Insurance Number (NINO) in terms of applications, given that neither SSN nor NINO contain biometric details and their use is restricted to only federal agencies,” says a CLSA report on the fintech industry.

In fact, regulations and records in India have undergone a tremendous transformation in recent years, particularly with the rise of fintech innovation. However, what sets India's BFSI sector apart is its unique reg-tech innovation, where government regulations are working hand in hand with fintech innovation to drive not just technological enhancements, but also a cultural change in the industry.

-

As more individuals and small and medium-sized enterprises become part of the formal financial ecosystem, fintech companies are poised to become primary drivers of this formalisation

Abhishant Pant, founder, The Fintech Meetup

BFSI companies are striving to incorporate digital solutions to streamline their operations and provide seamless customer experiences. One of the key players in India that provides the baseline stack around Identity and Digital Signatures is eMudhra. According to V Srinivasan, executive chairman of eMudhra, the company has been enhancing its identity and signing services by offering more forms of identities that can power eSign, which is leveraged by several fintech players.

V Srinivasan, explains that fintech innovation in India's BFSI sector is focused on facilitating digital services that drive ease and assurance in lending and other documentation-heavy processes. As the government increasingly allows more processes to go digital, more fintech companies are entering the industry to drive innovation on top of core services. Srinivasan emphasises the importance of tech innovation in BFSI and highlights the potential of digital services such as eSign, eStamping, eBank Guarantees, and digital branch initiatives.

"In recent years, banking and financial services in India have been transformed. The uniqueness of innovations in the BFSI sector in India does not merely lie in the fact that it is a product or tech innovation, but rather, a reg-tech innovation where government regulations go hand in hand with fintech innovation to drive not just a tech enhancement but also a cultural change in the industry. While there are many facets to fintech innovation in BFSI, we see a lot of process and tech innovation around facilitation of digital services that drive ease and assurance in lending processes (and increasingly, other documentation-heavy processes). More Fintech companies are entering the industry in an effort to drive innovation on top of core services like eSign, eStamping, eBank Guarantees & Digital Branch initiatives, as governments increasingly allow more processes (and in fact, mandates) to go digital,” says V Srinivasan.

In addition, eMudhra has been working towards consolidating its digital offerings in one platform to drive ease of adoption of such technologies, especially for larger BFSI entities. Srinivasan believes that the next advancement in adoption of digital transformation will evolve from digitisation of customer touchpoints to digitisation across the entire organisation. In this regard, eMudhra has already built a specific product for BFSI and is in discussion with key industry participants.

Ever expanding in scope

As per a Frost and Sullivan report, there are more than 1,860 fintech start-ups operating in the country, focusing on areas such as payments, lending, wealthtech, insurtech, and neo-banking. These start-ups have already secured more than a quarter of all start-up funding in India, and the fintech sector is set to attract even more investment in the near future.

Moreover, India's fintech market is projected to see impressive revenue growth in the coming years, with estimates suggesting that it could soar to Rs1,12,374.2 crore by 2027, up from Rs28,703.3 crore in 2021. This expected surge is primarily due to government policies supporting fintech innovation, increasing investments, and a high fintech adoption rate of 87 per cent, the highest compared to other countries.

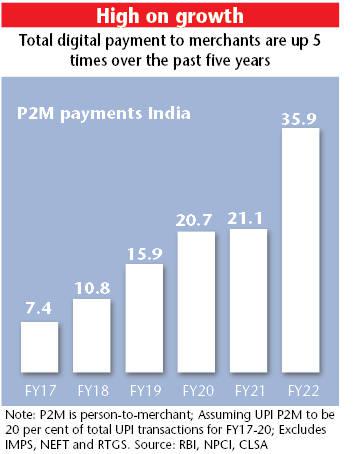

In payments alone, there is a vast opportunity for players. The fintech payments industry is witnessing a surge in real-time account-to-account (A2A) payments, phasing out cash and giving rise to innovative payment solutions. Payment gateways and aggregators, as well as point-of-sale providers, are now expanding beyond payment acceptance, offering full-stack merchant solutions. Moreover, the emergence of faster cross-border payment options is revolutionising the space.

-

There is a growing demand for solutions that address areas such as regulatory compliance, risk management, payment processing, and customer engagement

Hitesh Sahijwala, Executive vice president, India sales and distribution, Lentra

Fintech payment players operate across a diverse range of sub-segments, catering to different target audiences and business models. From consumer-focused platforms to merchant-centric solutions, fintech companies are redefining the landscape with their versatile offerings.

Further, there are ample opportunities for start-ups to flourish by targeting niche markets with innovative business models. Lending, for instance, presents a variety of options, from marketplace lenders to full-stack lenders. Meanwhile, digital payments boast collection platforms and evolved Buy-Now-Pay-Later (BNPL) players, each offering unique value propositions.

In fact, the payments space itself is incredibly diverse and is further divided into sub-segments such as app-based platforms, point-of-sale (POS) systems, payment aggregators (PA), and payment issuers. Each of these sub-segments has its own unique characteristics and target audiences, and many players in this space have managed to carve out a niche for themselves through differentiated products and innovative strategies.

For example, app-based payment platforms like Paytm and PhonePe have become household names in India, thanks to their user-friendly interfaces and seamless integration with popular services like Uber and Zomato. Payment aggregators like Razorpay and CCAvenue have also gained significant traction in recent years, as more and more businesses seek to streamline their payment processes and accept payments online.

Embedded lending options for consumption financing, digitisation of asset-backed lending, and experimentation with decentralised finance (DeFi) are other segments that are growing fast. As CLSA’s report suggests, assuming that fintechs expand the customer base by another 20 million, the lending opportunity in just personal loans with a ticket size of Rs1 lakh could skyrocket to as high as Rs2 lakh crore. Merchant loans are another significant opportunity.

One such innovative company is Navi Technologies, which focuses on India's digitally connected, young, middle-class population. With a mobile-first approach and strong in-house technology, Navi has expanded its offerings under the ‘Navi’ brand to include personal loans, home loans, general insurance, and mutual funds.

Wealthtech, the dynamic fusion of wealth management and technology, is taking the fintech world by storm. These trailblazing businesses have disrupted the status quo, offering digital products and services to address the investment, savings, and trading needs of customers in ways never before imagined.

The wealthtech revolution began with the rise of discount brokers, who shunned brick-and-mortar branches and conducted all operations online. As time progressed, this innovative concept extended into parallel segments, such as financial product advisory, distribution, and robo-advisory.

Not only have standalone wealthtech players risen to prominence, but large payment companies like Paytm have also ventured into the fray. Over the past 5 years, discount brokers have upended the retail equity broking segment with their irresistible product offerings and game-changing pricing models. In fact, the three largest brokers by active client count are fintech businesses: Zerodha, Upstox, and Groww.

Online brokers that allow investors to invest in overseas market have also been flourishing. “For Vested Finance, an online investment platform enabling Indian investors to invest in the US stock markets, witnessed trading volumes grow by 42 per cent in 2022 as compared to 2021 (the expected value of transactions for 2022 will be close to $250 million). Investors continued to be net buyers with buy volume 2x of sell volumes during the same period. This growth is driven by factors such as rising smartphone penetration, increasing internet usage, and the government's push toward digital payments and financial inclusion,” says Viram Shah, co-founder and CEO, Vested Finance.

-

Insurance, too, is a dynamic segment with full-stack insurtech players and marketplace players vying for dominance. Insurtech is the expansion of digital non-life insurers and bite-sized insurance, and the rise of digital platforms for insurance distribution. Policybazaar has been carving a niche in insurance distribution.

“Digital insurance sales are in a nascent stage, with a low-single digit share of overall insurance sales in India (using various measures). However, the market is quickly picking up, especially in products linked to protection and prevention. Consumer preference is shifting towards simpler products with clear communication, seamless online searches and transactions and hassle-free claims. All of these factors signal significant growth opportunities for insurtech firms,” says CLSA in its fintech report.

The SaaS fintech leap

One area of fintech that has seen significant growth is Software as a Service (SaaS). This model allows companies to access powerful software solutions without the need for expensive in-house development and maintenance. As fintech SaaS solutions continue to gain popularity, the market size for this segment in India is projected to grow to $12.6 billion by 2025, up from $4.6 billion in 2022.

“The fintech opportunity in the SaaS segment is significant,” says Hitesh Sahijwala, executive vice president, India sales and distribution, Lentra. “There is a growing demand for solutions that address areas such as regulatory compliance, risk management, payment processing, and customer engagement,” he notes. Lentra, a leading fintech SaaS company, is focusing on upgrading its cloud-powered platform after raising $60 million in Series B funding in November 2022. “We plan to acquire software teams focusing on various product engineering roles, such as Java, Open Software, and Risk Models that will help us re-engineer our platform with advanced upgrades.”

Another SaaS platform, Zaggle is a leading player in spend management, providing a differentiated value proposition and serving a diversified user base, according to a Frost & Sullivan report. Founded in 2011, Zaggle operates in the business-to-business-to-customer segment and stands out as one of the few uniquely positioned players offering a wide range of financial technology products and services. Its portfolio includes one of the largest numbers of issued prepaid cards in India, accounting for 12.7 per cent of the country's total prepaid transaction value as of 31March, 2022, as well as various software solutions like tax and payroll software.

“Fintech players in India are increasingly focusing on the employee-oriented services market as this segment of customers is easy to acquire and retain at lower costs. There were 2.23 million companies registered in India as of September 2021. The overall market for spend management software SaaS fee (in-house and outsourced; including procurement management, expense management, and payroll management) was estimated to be Rs8,180 crore in 2021, with the share of outsourced spend management being around 37 per cent (Source: Frost & Sullivan report). Our primary customers provide us with access to their employees, channel partners and customers, giving us the benefit of a diversified user base,” says Avinash Gokhundi, MD and CEO, Zaggle Prepaid Ocean Services.

Further, a new innovation in fintech is the distribution-as-a-service (DaaS) network. With robust, adaptable, multilingual apps, form factor agnostic devices and distribution tech, fintechs like PayNearby are working towards making India financially inclusive.

-

The use of AI in credit assessment clubbed with solutions like the account aggregator framework will help fintech improve efficiency and ensure access to credit where it is most needed

Sumit Chanda, CEO, and Founder of JARVIS Invest

“With our DaaS network, services spanning banking to e-commerce, digital entertainment and online education to insurance, travel to simple lending options are reaching the unserved and underserved areas of the nation. By making these services available at a nearby store, we are gradually bringing all at the last mile into the formal financial fold. We are revolutionising the retail ecosystem in the country and ensuring the sustainability and growth of small retailers with increased revenue,” says Bajaj of PayNearby, with the start-up created to make financial services available to everyone, everywhere, at a store nearby while empowering local retailers in the process.

What next for fintech?

“In FY23-24, the industry is likely to witness an increase in innovations within the remit of regulation. Fintech companies will need to bundle financial services while driving differentiation. Offering an unparalleled customer experience will be key to achieving market leadership,” says Sashank Rishyasringa, co-founder and MD, axio (formerly Capital Float).

In today's dynamic global economy, fintech companies are striving to utilise cutting-edge technologies like AI and machine learning to enhance efficiency, reduce costs and stay ahead of the curve. Collaborating with traditional banks to serve the large unbanked and underserved population in the country will become vital for fintech companies to establish themselves as leaders in the financial services industry.

Fintech firms must find more ways to effectively exchange data with traditional financial institutions. This is where protocols like UPI, GST, Account Aggregator, DigiLocker, and more come into play. According to Abhishant Pant, founder of The Fintech Meetup: “Leveraging digital public infrastructure like UPI, GST, Account Aggregator, DigiLocker and a few more like OCEN and ONDC which are in the initial phases have led to establishing a protocol and exchange of data between fintechs and financial institutions in a consumer consent-driven architecture which will bring the next level of fintech adoption.”

In fact, the Account Aggregator platform is a significant jump for fintech. “This past year has seen significant growth in the Account Aggregator (AA) ecosystem in India, with 1.1 billion AA-enabled accounts and 2.05 million users voluntarily sharing their financial data with banks and financial institutions. The AA framework is a game-changer for financial inclusion because it gives businesses access to the information they need to source, underwrite and manage portfolios more quickly and with a better user experience,” says Rishyasingra of axio.

That said, innovation in technology will also drive fintech forward. As AI/Machine Learning continues to grow and evolve, it will become increasingly important for fintech companies to leverage these technologies to stay ahead of the curve.

According to Jaya Vaidhyanathan, CEO of BCT Digital, there are two major trends that will shape the future of fintech: the increased application of AI/ML and the funding slowdown that the industry seems to be going through.

“The science of AI/ML has been growing at a tremendous pace,” says Vaidhyanathan. “However, the real-world application of the same has not scaled up at even a fraction of that speed. There is so much that can be done with AI/ML algorithms, but is not getting done because of the lack of past data to train the models. As mentioned above, the digitalisation of finance has been adding to the universe of data every day, and it is only a matter of time before we see increased application of AI/ML for banking use cases, like the effective and early detection of frauds.”

-

Going forward, fintechs which can transition to profitable models in the short to medium term will attract fresh capital in the next 1-2 years

Shachindra Nath, Vice Chairman and Managing Director, UGRO Capital

With the advancements in technology and a shift towards a more tech-savvy consumer base, fintech is also the hotbed of innovation. The industry is buzzing with new ideas and solutions that promise to disrupt traditional finance. One of the key innovations that is shaping fintech is hyper-personalised solutions. As Sumit Chanda, CEO, and Founder of JARVIS Invest, points out: “Hyper-personalised solutions will be the game changer.”

Neobanks, or digital-only banks, have been at the forefront of this trend, offering tailored solutions to their customers. The neo-banking industry is expected to reach a whopping $215 billion this year. With the rise of the young working population, there is an increased demand for personalised solutions, and traditional banks are taking notice, with many opting to partner with neobanks to offer their customers a more customised banking experience.

Another innovation that is shaping fintech is the use of AI in digital lending. Buy Now Pay Later, instant loans, and digital lending have become increasingly popular, but the banking sector’s ability to manage the demand for credit, ensure the quality of loans and maintain adequate capital buffers has been questioned. With the help of AI and the account aggregator framework, fintech companies can improve efficiency in credit assessment and ensure access to credit where it is most needed. As Sumit Chanda states: “The use of AI in credit assessment clubbed with solutions like the account aggregator framework will help fintech improve efficiency and ensure access to credit where it is most needed.”

However, when it comes to lending, one of the keys to success is continuous credit monitoring and robust credit risk assessment. Fintech has revolutionised the way traditional financial institutions assess credit risk by leveraging digital technologies such as AI and machine learning. As more financial institutions invest in these technologies to acquire customers, it is important to consider the developments that happen over the customer lifecycle.

“Consider the host of developments that happen over the lifecycle of the relationship between a customer and the institution. Continuous, automated monitoring is required to predict credit risk and fraud likelihood. This will be the differentiator among financial institutions going forward, in the context of the health of the asset book. This presents a great opportunity to the fintech sector. We are geared for this with a full lifecycle stack for credit, built in a modular, scalable manner. A greenfield institution can adopt our entire suite readily, while an established one with legacy systems can just add the missing capabilities – which is far less expensive than a rip-and-replace job,” notes Vaidhyanathan.

Challenging environment

One trend Vaidhyanathan believes will shape the future of fintech is the funding slowdown that has hit the fintech industry. “Easy monetary policies by the US Fed over the past years have distorted the fintech market,” says Vaidhyanathan.

“Every run-of-the-mill player in fintech has access to funding, thereby making it difficult for financial institutions to choose the right partner. However, eventually, as free money is no longer accessible, only the serious fintech players with innovative business models and good market acumen will thrive in the market.”

-

Due to the pandemic, UPI was pushed into the economy. The acceptance of UPI revolutionised digital payments, lending and credit

Nalin Agrawal, Co-founder & CEO of Snapmint

This development is good news for everyone involved in the fintech industry. For fintech companies, it translates to less, but genuine competition that promotes innovation. For financial institutions, it means fewer vendors to choose from, making it easier to identify and partner with the right fintech companies. And for customers, it means they have the option to select only from service providers that are deemed credible.

There are more hurdles to overcome in the form of financial literacy and cybersecurity. “Among the various cybersecurity concerns and increased regulatory scrutiny, I feel the major challenge the Indian fintech sector is still dealing with is financial literacy. Due to a lack of financial awareness, adequate education, and language barriers, citizens at the last mile take longer to understand the benefits that financial products can provide to make their lives easier. To improve operational effectiveness and better customer reach, fintechs have adopted cutting-edge technology, but the pace of technology adoption has not been proportional to its potential, leading to a gap in the penetration of financial services,” says Bajaj of PayNearby.

Future is fintech

In a world where fintech has revolutionised the financial landscape, millions of people now have access to financial services, elevating their economic status like never before. The focus on accessibility and simplified financial products is reshaping the very essence of how financial services are delivered. In fact, fintech has made it possible for investors to open demat accounts, which are at a record high, and growing.

The potential for fintech is staggering. As collaborations between banks, financial intermediaries, and fintechs flourish, these partnerships hold the key to bridging the nation’s digital and financial divide. By offering streamlined, easy-to-consume financial saving and investing products, fintechs are democratising banking and crafting sustainable financial models for the masses. Fintech pioneers are now making the once seemingly impossible possible, and driving the creation of a more financially inclusive India.

India is also a model for open banking deployments worldwide, and swiftly adapting newer technologies. The combined efforts of financial institutions, start-ups, the government, venture investors, and regulators have cultivated an environment ripe for innovation and expansion in the fintech space.

As we peer into the future, it’s clear that the fintech industry is on the cusp of even greater innovation and growth. As new players enter the fray and existing ones broaden their offerings, competition will inevitably intensify. But with a keen focus on customer needs, strong partnerships, and technology to drive efficiency and build scale, fintech companies can continue to create new opportunities and champion positive change in the financial sector. Ultimately, this will benefit consumers, and the economy as a whole.

-

As digitalisation forges ahead, fintech is breaking new ground in Bharat, ushering the underserved and unserved into a brave new world of access and awareness, and revolutionising consumer behaviour at the grassroots level

Anand Kumar Bajaj, Founder and MD, PayNearby

According to Muzammil Patel, Global Head Strategy and Corporate Finance at Acies: “The biggest challenges are expected to arise on the regulatory front. As traditional models are changed, points of supervision and control for regulators also change. This then leads to restrictive regulations until regulators fully understand the business models and are geared up for managing systemic risk. It will become increasingly important for fintechs to explain their models to regulators earlier on in their journey, self-regulate until regulations catch up and proactively offer themselves to regulatory oversight.”

“Over the last 2 years, the fintech industry overall is seeing consolidation with more focus on growing core profitability. New equity investments in start-ups have also slowed down in the last few quarters. Going forward, fintechs which can transition to profitable models in the short to medium term will attract fresh capital in the next 1-2 years,” feels Shachindra Nath, Vice Chairman and Managing Director, UGRO Capital.

Finally, with the advent of 5G, experts foresee a monumental shift in the delivery of financial services. Technologies like AI, IoT, cloud computing, quantum computing, and blockchain are poised to grow the industry further by leaps and bounds. The launch of 5G is expected to enable high-end trading and quicker distribution of fintech services, opening up new possibilities for the industry. The question is: how will these new technologies shape the future of finance in India and beyond? Only time will tell, but one thing is for sure – India's fintech industry is poised for continued growth and innovation.

In fact, the fintech revolution is not just a fleeting trend; it represents a seismic shift in our approach to finance, with the power to forge a more inclusive and prosperous future for all.